Philippines Agritech Input E-Marketplaces Market Reaches USD 1.2 Billion | Ken Research

The Philippines agricultural supply chain is being rewired from the bottom up. 60% of Filipino farmers now use online platforms for input transactions, a structural shift that is pulling seeds, fertilizers, pesticides, and farm machinery procurement onto digital marketplaces at scale. As per Ken Research analysis, the Philippines Agritech Input E-Marketplaces Market is valued at USD 1.2 billion in 2024, with a 40% increase in online farmer transactions recorded in recent years. The full competitive landscape is detailed in the Philippines Agritech Input E-Marketplaces Market Report.

This analysis draws on data from market intelligence modelling, Philippines Department of Agriculture disclosures, Agricultural Modernization Act policy data, and independent agritech sector benchmarking.

USD 1.2 Billion Market at 40% Online Transaction Growth: What Is Driving Platform Adoption

Smartphone penetration and mobile wallet adoption are the primary catalysts reshaping how the Philippines' 10 million smallholder farmers access agricultural inputs. Per industry survey data, over 50% of Filipino farmers have adopted mobile wallets, enabling frictionless payment for seeds, fertilizers, and pesticides on digital platforms. The government has allocated PHP 2 billion (approximately USD 36 million) toward agritech innovations under the Agricultural Modernization Act, creating a structured procurement pipeline for platform operators. Fertilizers and seeds remain the two dominant categories by transaction volume. Benchmark data for Southeast Asian agritech e-commerce can be found in the Southeast Asia Agritech Market intelligence report.

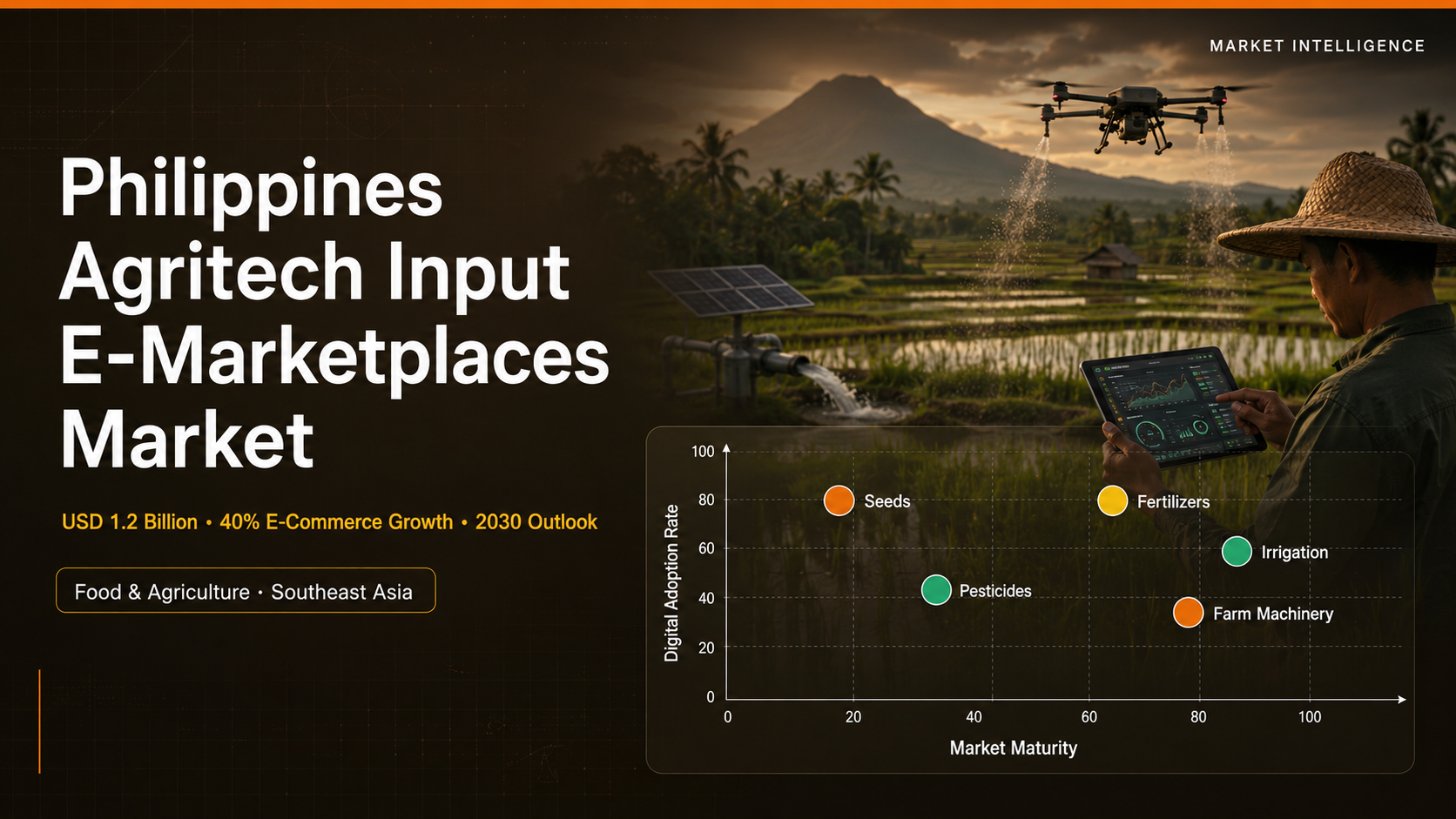

- Seeds and Fertilizers: Dominant input categories, now transacted online by 60%+ of platform-active farmers, reducing dependence on physical agri-input dealers.

- Pesticides and Crop Protection: Fast-growing digital procurement segment, driven by access to verified suppliers and price comparison tools not available at rural retail level.

- Farm Machinery and Irrigation: Emerging e-marketplace category as government subsidies enable smallholder access to equipment priced above PHP 100,000 per unit.

Syngenta, Bayer, and East-West Seed Lead as Digital Platforms Reshape Input Distribution

The Philippines agritech input e-marketplace is attracting both global agrochemical majors and home-grown digital platforms competing for distribution scale. Per market modelling, cooperatives represent approximately 30% of farmers, making them the single largest institutional buyer group on emerging digital platforms. Syngenta Philippines, Bayer CropScience AG, and Corteva Agriscience anchor the supply side, while East-West Seed Company commands a dominant position in the seeds category with 70%+ brand awareness among smallholder farmers across Luzon and Visayas. Homegrown platforms including AgriLink, FarmOn, Cropital, and SeedWorks Philippines are aggregating smallholder demand in rural provinces where physical distributor reach is thin. A useful comparative view of digital agriculture platforms across the region is available in the Indonesia Agritech Market report.

- East-West Seed Company: Dominant seeds supplier with deep cooperative relationships across Luzon, Visayas, and Mindanao, anchoring high-repeat-purchase categories on digital platforms.

- Syngenta Philippines and Bayer CropScience: Supplying certified crop protection inputs through both platform and distributor channels, leveraging regulatory compliance as a brand differentiator.

- AgriLink and FarmOn: Aggregating rural smallholder demand by integrating mobile payment rails, advisory services, and verified input sourcing into a single platform experience.

Which input category holds the highest gross margin on Philippines agritech e-marketplaces? Download Sample Report for segment-level pricing and competitive benchmarks.

Why 40% of Rural Areas Still Offline Creates the Market's Defining Challenge and Opportunity

The Philippines agritech e-marketplace market faces a structural tension: 40% of rural areas still lack reliable internet access, limiting platform reach precisely in the regions with the highest smallholder density. Yet this gap is also the primary investment thesis driving telco infrastructure expansion and government connectivity programs targeting agricultural provinces. Per industry estimates, technology adoption costs still exceed PHP 100,000 per farm for full digital input procurement integration, creating a financing barrier that cooperative models and government subsidy schemes are actively addressing. The 30% increase in organic farming practices since 2020 is generating a premium input procurement channel, pulling higher-margin certified organic seeds and soil amendments onto platforms ahead of commodity inputs.

Philippines Agritech Input E-Marketplaces Outlook to 2030: Three Structural Drivers

The government's target of 1 million hectares under certified organic farming by 2030 will reshape input procurement toward verified, traceable supply chains that only digital platforms can provide at scale. Per market intelligence benchmarking, 50% of Filipino farmers have already adopted mobile wallets, creating the payment infrastructure that converts offline buyers into recurring platform users. The expansion of cooperative digital procurement programs across Mindanao, where agricultural density is highest, is the next major volume unlock. Investors tracking adjacent Philippines agricultural sectors should also review the Philippines Agriculture Market for macro demand context.

- Government Agricultural Modernization Act: PHP 2 billion agritech allocation providing structured procurement demand for registered platform operators and certified input suppliers.

- Mobile Wallet Penetration: 50%+ farmer adoption of GCash and Maya creating low-friction payment rails that directly enable rural smallholder platform participation.

- Organic Farming Expansion: Government target of 1 million hectares organic by 2030 driving premium input procurement onto certified digital supply chains.

Ready to map agritech platform strategy against the Philippines' 2030 digital agriculture targets? Philippines Agritech Input E-Marketplaces Market Report delivers segment forecasts and competitive benchmarks.

Conclusion

The Philippines Agritech Input E-Marketplaces Market is at an inflection point where mobile wallet infrastructure, government modernization funding, and cooperative digitization are converging to pull the majority of smallholder input procurement onto digital platforms before 2030. Platforms that solve the last-mile connectivity barrier and the PHP 100,000+ technology adoption cost will capture the highest-frequency, highest-loyalty farmer segments. Access the Philippines Agritech Input E-Marketplaces Market Report for the full competitive landscape.

Frequently Asked Questions

Q1: What is the size of the Philippines Agritech Input E-Marketplaces Market?

The market is valued at USD 1.2 billion in 2024, with a 40% increase in online farmer transactions recorded in recent years, driven by mobile wallet adoption and government agritech funding of PHP 2 billion.

Q2: Who are the key players in the Philippines Agritech Input E-Marketplaces Market?

Leading players include Syngenta Philippines, Bayer CropScience AG, Corteva Agriscience, East-West Seed Company, AgriLink, FarmOn, and Cropital. Cooperatives representing 30% of farmers are the largest institutional buyer group on digital platforms.

Q3: Which segment leads the Philippines Agritech Input E-Marketplaces Market?

Seeds and Fertilizers are the dominant categories by transaction volume, with 60%+ of platform-active farmers now transacting these inputs online. Farm machinery is the fastest-growing category as government subsidies expand access to equipment above PHP 100,000 per unit.

Q4: What is driving growth in the Philippines Agritech Input E-Marketplaces Market?

Three drivers compound: 50%+ mobile wallet adoption among farmers enabling frictionless digital payment, government allocation of PHP 2 billion for agritech modernization, and a 30% rise in organic farming since 2020 driving premium input procurement onto certified platforms.

Q5: What challenges does the Philippines Agritech Input E-Marketplaces Market face?

The primary challenge is the connectivity gap: 40% of rural areas still lack reliable internet access, limiting platform reach in high-density smallholder regions. Technology adoption costs exceeding PHP 100,000 per farm also constrain uptake without cooperative financing or government subsidy support.

For the full competitive benchmarking, segment-level forecasts, and regional breakdown, access the Philippines Agritech Input E-Marketplaces Market Report from Ken Research, a leading market intelligence firm covering food and agriculture markets across Southeast Asia.