APAC Social Commerce Market Hits USD 625B on Livestream and TikTok Shop Wave | Ken Research

The defining shift in APAC social commerce is not coming from traditional marketplaces. It is coming from a livestream and short-video commerce wave, anchored by China's USD 4.7 trillion 2030 forecast and Southeast Asia's TikTok Shop adoption. As per Ken Research market modelling, the APAC Social Commerce Market is valued at USD 625 billion in 2024, with the region capturing 71.6% of the global social commerce market. The complete country split, platform share, and segment forecast are in the APAC Social Commerce Market Report.

This analysis draws on data from Ken Research market modelling, IMDA Singapore digital economy disclosures, regional platform GMV announcements, and independent e-commerce sector benchmarking.

USD 625B Market: APAC at 71.6% of Global Social Commerce Share

The regional dominance is structural. As tracked by Ken Research modelling, APAC accounted for 71.6% of the global social commerce market in 2024, with China alone forecast to reach USD 4.7 trillion by 2030 at a 33.5% CAGR. Live commerce, group buying, and influencer-led product discovery now anchor consumer journeys across the region. For investors mapping adjacent emerging-market commerce, the Indonesia Social Commerce Market shows the same livestream-led adoption now compounding across Southeast Asia.

- Global dominance: APAC at 71.6% of global social commerce share, anchored by China, Southeast Asia, and South Asia.

- China lift: China's social commerce forecast at USD 4.7 trillion by 2030 at a 33.5% CAGR.

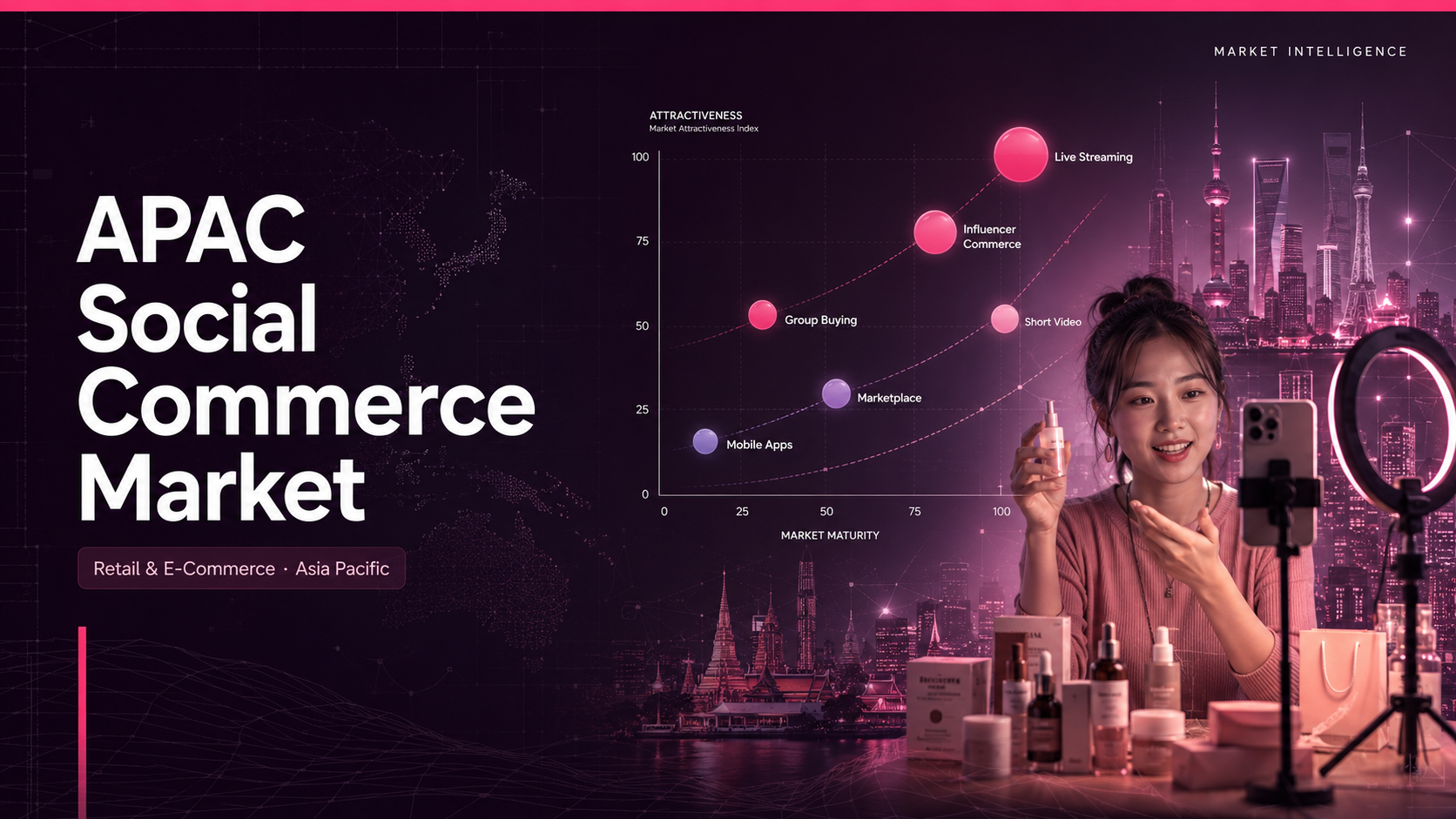

- Historical CAGR: APAC social commerce compounded at 12.6% CAGR from 2021 to 2024.

TikTok Shop, Shopee, Alibaba and Lazada Anchor APAC Platform Stack

The platform map is layered across China-native and Southeast Asia leaders. As estimated by Ken Research, Alibaba, Pinduoduo, JD.com, Douyin and TikTok Shop (ByteDance), WeChat (Tencent), and Kuaishou dominate China, while Shopee (Sea), Lazada (Alibaba), Meta/Instagram, and Pinterest anchor Southeast Asia. Live commerce growth and influencer-led discovery are reshaping consumer journeys, per the Singapore IMDA digital economy framework. The platform stack rewards integration with creator and livestream tooling.

- China leaders: Alibaba, Pinduoduo, Douyin, and WeChat anchor the world's deepest social commerce stack.

- SEA leaders: Shopee, TikTok Shop, and Lazada lead Indonesia, Vietnam, Thailand, and Philippines.

Need the country-by-country social commerce share across China, Indonesia, Vietnam, India, and Thailand plus livestream segment forecast? Download Sample Report for platform GMV and segment-level forecasts.

Why Is Livestream Commerce Reshaping APAC Shopping Behaviour by 2030?

Live commerce, initially driven from China, is now mainstream across Southeast Asia and South Asia. According to Ken Research analysis, livestream conversion rates outperform traditional e-commerce by significant margins, lifting platform GMV per session. YouTube and Shopee partnership in Indonesia exemplifies the cross-platform integration trend, enabling in-video purchases. Influencer creator economies are now structural across China, Indonesia, Vietnam, and India. The combined effect is a re-pricing of digital advertising budgets toward creator-led platforms through 2030.

APAC Social Commerce Outlook to 2030: USD 625B Base, 8% CAGR Lift, and China Anchor

Three drivers anchor the forward view. Per Ken Research modelling, APAC social commerce expands at around 8.1% CAGR from 2025 to 2030, with China as the structural anchor. For investors tracking adjacent digital-ad spend, the Brazil Digital Advertising and Retail Media Market shows the same retail-media build-out compounding social commerce globally.

- Regional CAGR: APAC at around 8.1% CAGR from 2025 to 2030, with China at 33.5% on a much larger base.

- Platform integration: YouTube-Shopee Indonesia partnership exemplifies cross-platform in-video purchase flows.

- Influencer economy: Creator-led discovery anchors Indonesia, Vietnam, and India growth.

What Brands, Platforms, and Investors Must Do Before TikTok Shop Consolidation Closes

The combined effect of TikTok Shop expansion, Shopee Live integrations, and Alibaba's China dominance creates a narrow positioning window. Brands, platforms, and capital allocators must move before the next round of livestream consolidation.

- Brands: Build creator and livestream-native commerce playbooks to capture 71.6% global share APAC consumer attention.

- Platforms: Lock cross-border SEA expansions to defend share against TikTok Shop's rapid Indonesia and Vietnam entry.

- Investors: Track creator-economy SaaS, livestream tools, and group-buying platforms scaling within APAC.

Mapping APAC social commerce expansion or planning a creator-economy investment? Access the APAC Social Commerce Market Report for platform share, country revenue split, and livestream forecasts.

Conclusion

APAC social commerce has entered a livestream-led inflection where China dominance, Southeast Asia adoption, and creator economies compound on the same platform stack. The brands and platforms that build livestream depth ahead of the 2030 reset will defend share rather than chase it. For brands and investors, the strategic question is no longer whether social commerce wins, it is who owns the next livestream commerce category. Access the APAC Social Commerce Market Report for the full landscape.

Frequently Asked Questions

Q1: What is the size of the APAC Social Commerce Market?

The APAC Social Commerce Market is estimated at USD 625 billion in 2024 per Ken Research market modelling, with the region holding 71.6% of global social commerce share across livestream, group buying, and influencer formats.

Q2: Who are the key platforms in APAC social commerce?

Leading platforms include Alibaba, Pinduoduo, JD.com, Douyin and TikTok Shop, WeChat, Shopee, Lazada, and Meta and Instagram. For broader emerging-market e-commerce parallels see the Middle East and Africa E-Commerce Market.

Q3: Which country leads APAC social commerce?

China leads with a forecast of USD 4.7 trillion by 2030 at a 33.5% CAGR per Ken Research estimates, followed by Indonesia, Vietnam, India, and Thailand as the fastest-growing SEA and South Asia markets.

Q4: What is driving growth in APAC social commerce?

Growth drivers include livestream commerce mainstreaming, TikTok Shop SEA expansion, YouTube-Shopee Indonesia integration, and creator-led discovery, with historical CAGR of 12.6% from 2021 to 2024.

Q5: How does livestream commerce affect APAC retail?

Live commerce delivers higher conversion than traditional e-commerce, lifting platform GMV per session and accelerating cross-border SEA expansion across Shopee Live, TikTok Shop, and Douyin platforms.

For the full competitive benchmarking, country-level forecasts, and platform GMV split, access the APAC Social Commerce Market Report from Ken Research, a leading market intelligence firm covering retail and e-commerce across Asia Pacific.