India Web Insurance Aggregator Market 2025-2030: USD 2.09 Bn at 12.2% CAGR

Executive Summary

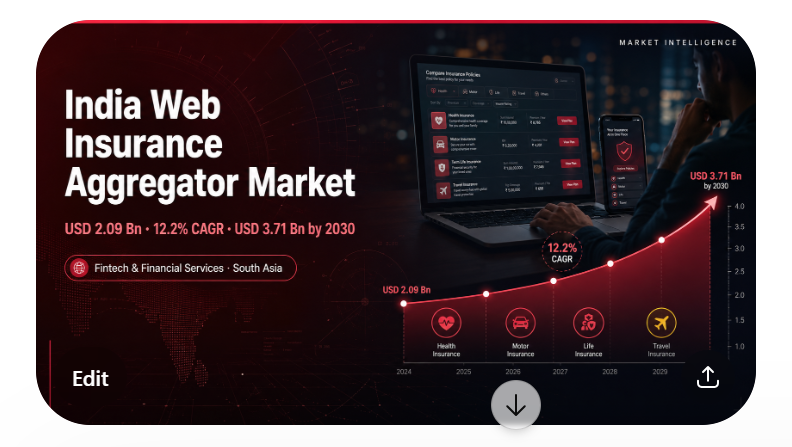

India's online insurance aggregator market reached USD 2.09 billion in 2025, tracking toward USD 3.71 billion by 2030 at a 12.2% CAGR. IRDAI's 2023 web aggregator guidelines, rising millennial insurance adoption, and PolicyBazaar's pivot to insurance broking are reshaping a sector that now processes nearly 25% of India's life insurance volume and over 7% of retail health cover.

Key Market Velocity Data

- Current Market Value: USD 2.09 billion in 2025, anchored by motor and health insurance comparison traffic

- Projected Market Value: USD 3.71 billion by 2030, driven by millennial adoption and smartphone insurance penetration

- CAGR: 12.2% during 2025 to 2030, among the fastest growth rates in India's financial services distribution sector

- PolicyBazaar Volume: Processes nearly 25% of India's life insurance and over 7% of retail health cover nationally

- Primary Growth Catalyst: Motor Vehicles Act 2019 amendment mandating third-party motor insurance, creating structurally captive aggregator demand from 300+ million registered vehicles

What Is Driving the India Insurance Aggregator Sector at 12.2% CAGR?

Three demand forces sustain the growth trajectory. Rising insurance awareness among India's millennial population is shifting policy purchases from branch-based distribution to digital comparison platforms that offer price transparency and instant policy issuance. The Motor Vehicles Act 2019 amendment mandating third-party insurance created a structurally captive demand base that aggregators capture through search traffic. IRDAI's 2023 guidelines on commission disclosure and fair comparison standards increased consumer trust in platform recommendations, reducing conversion friction that historically limited online insurance ticket values.

- New product category expansion: Growing demand for cyber insurance, travel insurance, renters' insurance, and pet insurance creates aggregator inventory breadth that drives repeat platform visits and cross-sell revenue beyond the core motor and health policy categories where incumbents built their user bases

- Foreign investor entry: International insurance technology investors have committed capital to Indian aggregator platforms, bringing underwriting data science and product innovation that widens the gap between tech-enabled aggregators and traditional broker distribution channels

- IRDAI regulatory modernization: The 2023 Insurance Web Aggregator guidelines mandate commission disclosure, fair comparison standards, and data privacy compliance, raising the operating standards that all IRDAI-licensed aggregators must meet and creating a regulatory moat against unlicensed comparison platforms

Which Entities Are Shaping the Competitive Landscape?

PolicyBazaar dominates as the market leader, processing nearly 25% of India's life insurance after obtaining a broking license in 2021 and building 100+ offline branches. CoverFox Broking, InsuranceDekho, and Turtlemint serve SME health and term life segments. Acko General Insurance and Go Digit represent insurtech challengers combining digital distribution with direct underwriting. The Insurance Regulatory and Development Authority of India (IRDAI) governs all licensed aggregators under Insurance Web Aggregators Regulations 2017, updated with 2023 commission disclosure guidelines.

- PolicyBazaar's omnichannel pivot: The platform's 2021 transition from pure aggregator to licensed broker, combined with its 100+ offline outlet expansion, signals that the high-ticket life and health insurance categories require human advisor touchpoints alongside digital comparison, creating a hybrid distribution model that pure-digital challengers cannot easily replicate

- Acko and Go Digit (direct insurtech): These platforms compress the value chain by combining digital aggregation with direct underwriting, potentially capturing margin from both sides of the insurance transaction, though they also carry underwriting risk that traditional aggregator-only models avoid by operating purely as distributors

What Does This Mean for B2B Decision-Makers?

The combination of 12.2% CAGR growth, IRDAI regulatory formalization, and PolicyBazaar's omnichannel pivot signals that India's insurance distribution is transitioning from a pure-digital aggregation model toward a hybrid broker-platform model requiring both technology investment and licensed advisor capacity. Companies that secure IRDAI aggregator or broker licenses in 2025 to 2026 and build category depth in underpenetrated segments like cyber and SME health will position for disproportionate share of the projected USD 3.71 billion market by 2030.

- For insurers seeking distribution: PolicyBazaar's 25% share of life insurance volume makes aggregator channel partnerships a first-priority distribution investment for any insurer targeting scalable digital customer acquisition at lower cost per policy than traditional branch networks

- For technology and platform investors: The 12.2% CAGR trajectory combined with IRDAI's 2023 regulatory formalization reduces platform licensing risk and creates durable barriers for compliant aggregators that hold IRDAI authorization, making licensed aggregator platforms attractively defensible assets

- For market entrants: InsuranceDekho and Turtlemint demonstrate that vertical specialization in SME health and term life creates high-LTV customer segments that commodity motor aggregation cannot match, signalling that niche positioning beats horizontal comparison breadth for profitable growth in the USD 3.71 billion target market

Ken Research Strategic Outlook

India's insurance aggregator market is transitioning from traffic arbitrage to advisory-led distribution. PolicyBazaar's offline pivot validates that high-ticket life and health insurance require human touchpoints alongside digital comparison, creating a model that digital-only entrants must replicate to access the premium ticket sizes driving market value growth. Ken Research analysis tracks that IRDAI's 2023 commission disclosure mandates will accelerate consolidation among unlicensed comparison platforms, leaving licensed brokers and aggregators with a regulatory advantage in the USD 3.71 billion market by 2030.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: India Web Insurance Aggregator Market Report