There is a requirement sitting at the center of AMC operations that does not get talked about nearly enough, and when it does come up, it is often misunderstood.

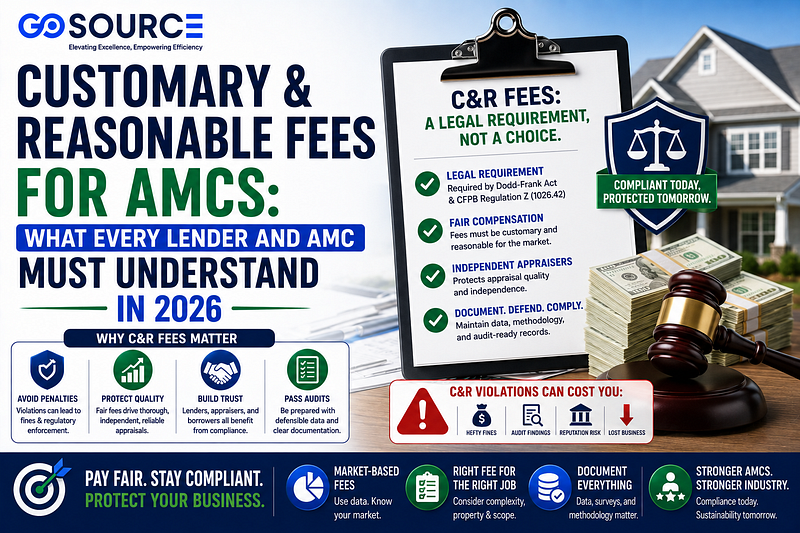

Customary and reasonable fees, commonly called C&R fees, are not a best practice or an industry guideline. They are a legal requirement established under the Dodd-Frank Wall Street Reform and Consumer Protection Act, enforced by the Consumer Financial Protection Bureau, and monitored by state regulators across the country.

The requirement is straightforward in concept: when an AMC hires an appraiser to complete an appraisal, the fee paid to that appraiser must be customary and reasonable for the type of appraisal being completed in the geographic market where the property is located.

In practice, C&R fee compliance is one of the most frequently mishandled areas of AMC operations and one of the most consequential when it goes wrong. Violations can result in civil money penalties, regulatory findings, lender audit failures, and reputational damage that is difficult to recover from.

This blog explains exactly what customary and reasonable fees mean, how violations happen, what the consequences look like, and what AMCs must do to stay compliant in 2026.

The Legal Foundation: Where C&R Fees Come From

To understand why C&R fees matter so much, it helps to understand where the requirement comes from and why it was created.

Before the 2008 financial crisis, the appraisal industry was plagued by fee pressure. Mortgage volume was high, competition among appraisers was intense, and lenders and AMCs frequently drove appraisal fees down to the lowest possible level. Appraisers who wanted the work accepted fees that did not adequately compensate them for the time and expertise required to complete a credible, independent appraisal.

The result was predictable. Appraisers under fee pressure took shortcuts. They rushed reports, selected favorable comparables, and produced valuations that supported loan amounts rather than reflecting genuine market value. This contributed directly to the inflated property values that helped fuel the mortgage crisis.

The Dodd-Frank Act responded to this directly. Section 1472 of Dodd-Frank, codified in CFPB Regulation Z Section 1026.42, established a clear rule: lenders and AMCs must pay appraisers’ fees that are customary and reasonable for the geographic market. The intent was to ensure that appraisers are compensated at a level that allows them to produce thorough, independent, high-quality work rather than being squeezed to the point where quality is compromised.

The rule also established that the fee paid to the appraiser and the fee charged to the borrower are separate considerations. An AMC’s technology fee, administrative fee, or management fee cannot come out of the appraiser’s compensation. The appraiser’s portion must stand on its own as customary and reasonable.

What “Customary” and “Reasonable” Actually Mean

The Dodd-Frank rule does not set up a specific dollar amount for appraisal fees; it cannot, because appraisal fees vary significantly by property type, geographic market, loan type, and assignment complexity. Instead, it establishes a standard that fees must meet.

Under CFPB Regulation Z, there are two acceptable ways for an AMC to demonstrate that it is paying customary and reasonable fees:

Method 1: Fee surveys. The AMC relies on objective third-party information about fees paid to appraisers for similar appraisal assignments in the same geographic market. Acceptable sources include fee surveys published by government-sponsored enterprises, state agencies, or independent appraisal organizations. The fee paid must be consistent with what these surveys show for the same type of assignment in the same market.

Method 2: Presumption of compliance. The fee is presumed to be customary and reasonable if it meets two conditions simultaneously: the fee is reasonably related to recent rates paid for similar appraisal services in the geographic market, and the fee is not based on a prohibited factor such as the loan amount, the property value, or whether the transaction closes.

In practice, most AMCs use a combination of market knowledge, published fee data, and appraiser feedback to set fee schedules. The problem is that “market knowledge” is subjective, and without a documented, defensible methodology for how fees are set, AMCs are exposed when a regulator or auditor asks them to justify their fee structures.

How C&R Fee Violations Actually Happen

Understanding the specific ways C&R fee violations occur is important because many AMCs that are in violation do not realize it. The most common violation patterns are not the result of intentional wrongdoing; they are the result of operational practices that have not been scrutinized against the legal standard.

Pay below-market fees to maximize the AMC margin. The most direct form of violation is an AMC that sets appraiser fees artificially low to increase its own management fee margin. If the total fee charged to the borrower stays constant and the AMC’s portion grows while the appraiser’s portion shrinks, the appraiser may be receiving below-C&R compensation even if the borrower is paying a reasonable total fee. This is exactly the scenario Dodd-Frank was designed to prevent.

Failing to adjust fees for geographic market differences. C&R fees are market specific. An AMC that applies to a uniform national fee schedule without adjusting for regional market differences will be underpaying appraisers in higher-cost markets and potentially overpaying in lower-cost markets. The underpayment in high-cost markets is a C&R violation even if the fee would have been adequate in a different geography.

Not adjusting fees for assignment complexity. A standard 1004 appraisal in a suburban market with abundant comparable sales is a materially different assignment than a rural property on ten acres with sparse comparable data. C&R fees must reflect the complexity of the specific assignment. Paying the same fee for both assignments fails the C&R standard for the complex one.

Fee compression on rush orders. Some AMCs offer rush processing without increasing the appraiser fee, expecting appraisers to prioritize the assignment without additional compensation. If rush orders require more appraiser effort or scheduling disruption, the C&R standard may require a higher fee to reflect that added burden.

Technology fees that reduce appraiser compensation. As AMC platforms charge technology fees or portal access fees to appraisers either directly or by deducting them from the assignment fee, the net compensation received by the appraiser may fall below the C&R threshold even if the gross assignment fee appeared compliant. Regulators have scrutinized this practice specifically.

Not updating fee schedules to reflect market changes. Appraisal fee markets change over time. An AMC that sets its fee schedule based on 2022 market data and has not updated it to reflect 2025 or 2026 market conditions may be paying fees that are no longer customary and reasonable, even if they were compliant when originally established.

The Consequences of C&R Fee Non-Compliance

The consequences of C&R fee violations are real, specific, and documented. This is not a theoretical risk; regulators have acted against AMCs and lenders for C&R fee failures.

Civil money penalties. Under Dodd-Frank and CFPB Regulation Z, civil money penalties for appraiser independence and fee violations can reach significant amounts. First-time violations can result in penalties of up to $10,000 per day. Subsequent violations can reach $20,000 per day. For an AMC operating at meaningful volume, these penalties can accumulate quickly.

State regulatory action. Beyond federal enforcement, most states have their own AMC licensing requirements that incorporate C&R fee standards. State appraisal boards and financial regulators have authority to suspend or revoke AMC licenses for fee compliance failures; therefore, that would effectively shut down an AMC’s ability to operate in that state.

Lender audit findings. Lenders carry vendor management responsibility for their AMC partners. When a lender’s compliance team or an external auditor reviews the AMC’s fee practices and finds C&R violations, the finding goes on the lender’s record, not just the AMCs’. This creates direct incentive for lenders to vet their AMC partners’ fee practices before routing volume to them.

GSE compliance exposure. Fannie Mae and Freddie Mac have both incorporated appraisal independence and fee compliance into their seller/servicer guide requirements. Lenders delivering loans to the GSEs with appraisals produced under C&R-non-compliant fee arrangements are carrying loan-level compliance risk that can surface during GSE audits.

Appraiser attrition. Beyond the regulatory consequences, below-market fees drive quality appraisers off AMC panels. Appraisers who have options and the best appraisers always do will stop accepting assignments from AMCs that consistently pay below-market rates. The result is a panel that skews toward less experienced or less selective appraisers, which Drives Revision rates up, and report quality is down. C&R fee compliance is not just a legal requirement; it is a panel quality strategy.

What a Compliant C&R Fee Process Looks Like

Building a genuinely compliant C&R fee process requires more than good intentions. Here is what it looks like in practice.

Maintain documented, market-specific fee schedules. Fee schedules should be documented at the market level, ideally at the county or MSA level, and reflect current market rates for each appraisal type. The documentation should show the data sources used to establish the schedule and the date it was last reviewed and updated.

Use objective third-party fee data. Fee schedules should be grounded in objective, documented data sources, such as published fee surveys, GSE fee guidance, state appraisal board resources, or independent industry surveys. Relying on internal judgment alone is not a defensible methodology under regulatory scrutiny.

Review and update fee schedules regularly. Fee schedules should be reviewed at least annually and more frequently in markets where appraiser availability or market conditions are changing rapidly. A fee schedule that was compliant eighteen months ago may not be compliant today.

Document the separation between AMC fees and appraiser fees. Every file should clearly document what the appraiser was paid and what the AMC retained. The appraiser’s fee must be independently justifiable as customary and reasonable, not just what remains after the AMC’s portion is deducted.

Build fee adjustment logic for complexity and geography. The fee process should have built-in adjustments for rural assignments, complex property types, rush orders, and other factors that legitimately increase the appraiser’s burden. A flat fee schedule without adjustment logic cannot be fully C&R compliant across a diverse order mix.

Track and respond to appraiser fee feedback. Appraisers who consistently decline assignments citing inadequate fees are providing real-time market feedback on fee adequacy. AMCs that track declination patterns by market and fee level have an early warning system for C&R compliance gaps, and those that ignore this data are missing the most direct signal available.

What Lenders Should Be Asking Their AMC About C&R Fees

Lenders who route volume through AMCs share in the compliance of exposure when those AMCs are not meeting C&R requirements. The following questions should be standard in every AMC vendor evaluation:

- Can you provide documentation of your fee schedule methodology and the data sources used to establish it?

- How frequently are your fee schedules reviewed and updated?

- How do you document the separation between appraiser fees and AMC fees at the file level?

- Do your fee schedules include adjustments for rural markets, complex property types, and rush orders?

- What is your appraiser assignment declination rate, and how do you use that data to assess fee adequacy?

- Can you produce fee compliance documentation for a regulatory audit on request?

An AMC that cannot answer these questions with specific, documented responses is carrying C&R compliance risk and sharing that risk with every lender in their client portfolio.

How Go Source Valuation Supports C&R Fee Compliance

At Go Source Valuation, we understand that customary and reasonable fee compliance is not just a checkbox; it is the foundation of a sustainable, high-quality appraisal panel. Our back-office support infrastructure helps AMCs build and maintain fee structures that are defensible, market-specific, and regularly updated to reflect current conditions.

From fee schedule documentation to appraiser compensation workflow management, our team brings the operational discipline that C&R compliance requires, protecting both the AMC and every lender relationship they serve.

If your AMC wants to make sure its fee practices are fully compliant and audit-ready, we would like to help. Visit our AMC Management Solutions page to learn more about how Go Source Valuation supports AMC compliance and operational excellence.

Frequently Asked Questions

What are customary and reasonable fees for AMCs?

Customary and reasonable fees, commonly referred to as C&R fees, are the legally required standard for appraiser compensation established under Section 1472 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The standard requires that fees paid by AMCs to appraisers must be consistent with fees paid for similar appraisal assignments in the same geographic market, ensuring appraisers are compensated at a level that supports independent, high-quality work.

Where does the C&R fee requirement come from legally?

The C&R fee requirement comes from the Dodd-Frank Wall Street Reform and Consumer Protection Act, specifically Section 1472, which is implemented through CFPB Regulation Z Section 1026.42. It was created in response to the appraisal fee compression that contributed to the 2008 financial crisis by incentivizing appraisers to rush reports and support inflated values rather than provide credible, independent assessments.

Can an AMC deduct its technology or management fee from the appraiser’s compensation?

No. Under the Dodd-Frank C&R fee standard, the fee paid to the appraiser must be independently customary and reasonable; it cannot be reduced by deducting AMC technology fees, portal fees, or administrative charges. The appraiser’s compensation and the AMC’s fee must be treated as separate components, and the appraiser’s portion must meet the C&R standard on its own.

What are the penalties for C&R fee violations?

Civil money penalties for appraiser independence and fee violations under CFPB Regulation Z can reach up to $10,000 per day for first violations and up to $20,000 per day for subsequent violations. State regulators also have authority to suspend or revoke AMC licenses for fee compliance failures. Beyond financial penalties, violations create lender audit findings and GSE compliance exposure that can damage or end AMC-lender relationships.

How should an AMC document its C&R fee compliance?

AMCs should maintain documented, market-specific fee schedules grounded in objective third-party data sources such as GSE fee surveys, state appraisal board resources, or independent industry surveys. Documentation should show the data sources used, the date the schedule was established, and when it was last reviewed and updated. Every file should also clearly document the separation between appraiser fees and AMC fees.

How often should AMCs update their fee schedules?

Fee schedules should be reviewed and updated at least annually and more frequently in markets experiencing significant changes in appraiser availability, market conditions, or regulatory guidance. A fee schedule established on historical data that has not been updated to reflect current market rates may be non-compliant even if it was adequate when originally set.

Why do C&R fees matter for lenders, not just AMCs?

Lenders carry vendor management responsibility for their AMC partners under GSE guidelines and CFPB expectations. When an AMC’s fee practices are found to be non-compliant during a lender audit or regulatory examination, the finding can appear on the lender’s own compliance record, creating direct financial and regulatory exposure for the lender. This is why C&R fee compliance documentation should be a standard component of every AMC vendor evaluation.

How does C&R fee compliance affect appraisal panel quality?

Below-market fees drive the best appraisers away from AMC panels. Experienced, in-demand appraisers have the leverage to decline assignments from AMCs that consistently pay below market rates, and they use it. The result is a panel that skews toward less experienced appraisers, which drives revision rates up and report quality down. Paying customary and reasonable fees is both a legal requirement and a practical strategy for maintaining a high-quality panel.