In manufacturing, there’s a concept called the “dark factory,” a fully automated facility that runs 24/7 with the lights off because no human workers are present to need them. The idea seemed futuristic when it emerged in the 1980s. Today, companies like Philips and Fanuc run dark factories on scale.

The appraisal management industry is approaching its own version of this concept, and most AMC operators haven’t noticed it happening.

Call it the “dark AMC back-office.” Not a fully lights-out operation, but a model where most coordination tasks, credential checks, order status updates, quality flags, and panel management decisions are handled by intelligent automation with human staff reserved for exception handling, client strategy, and complex judgment calls.

This isn’t a distant forecast. It’s being assembled right now, one workflow at a time.

Why AMC Back Offices Are Ripe for Automation

AMC operations have several characteristics that make them exceptionally well-suited to AI-driven automation:

High volume, repeatable decisions. Order routing, appraiser assignment, status updates, and credential checks are performed dozens or hundreds of times per day. Each instance follows similar logic. This is exactly where automation delivers compounding returns.

Structured data inputs. Appraisal orders arrive with property addresses, loan types, lender requirements, and delivery deadlines, clean, structured data that AI systems can immediately parse and act on. And with UAD 3.6 standardizing appraisal report data further, the structured format will reduce the unstructured free text that previously made automation harder and less reliable.

Clear performance metrics. Turn time, revision rate, appraiser quality score, and SLA compliance are measurable, trackable, and optimizable. Automation systems thrive when success is quantifiable.

Compliance-driven workflows. AIR requirements, USPAP standards, and GSE guidelines mean many AMC decisions aren’t judgment calls; they’re rule-governed. Rule-governed processes are the first to be automated.

What the Dark AMC Back-Office Actually Looks Like

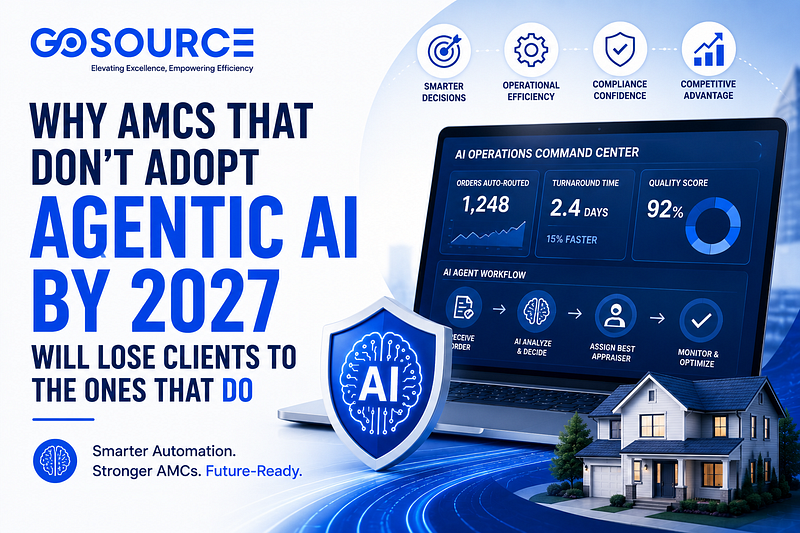

Picture a mid-sized AMC managing 800 active orders at any given time. Today, that typically requires a coordinator team handling assignment queue, a quality review team chasing revisions, an operations manager monitoring SLA dashboards, and an admin team managing appraiser credentials and lender communications.

In a dark back-office model, those functions are restructured:

Automated order intake and routing handles assignment decisions using multi-variable scoring: appraiser geography, license status, current workload, historical quality score, property type experience, and GSE-specific requirements. No coordinator touches routine assignments.

Autonomous credential monitoring tracks every appraiser’s license expiration, E&O insurance renewal, and state registration status. Expiring credentials trigger automatic suspension from the assignment pool, direct outreach to the appraiser, and a coverage gap alert to operations 60 days before any expiration.

AI-assisted quality flagging reviews incoming appraisal reports against UAD requirements, GSE guidelines, and lender-specific overlays. Reports with common deficiencies, such as missing addenda, inconsistent adjustments, and comparable selection issues, are flagged automatically before a human reviewer opens them, with the specific concern pre-identified.

Intelligent lender communication monitors every order’s status against its SLA commitment. Orders at risk of missing deadlines trigger automated lender notifications with updated delivery estimates, pre-drafted in the lender’s preferred communication style.

What remains for the human staff? Exception of handling, complex ROV disputes, client strategy conversations, appraiser relationship management, and the judgment calls that require contextual reasoning, no AI system has yet mastered.

The result is an AMC that can handle significantly higher order volume with the same headcount or maintain the same volume with a leaner team and higher margin.

The Appraiser Scorecard as the Engine of Automated Intelligence

None of this works without clean, continuous appraiser performance data. The appraiser scorecard, often treated as a quality management tool, is the data engine that makes dark back-office automation possible.

A robust scorecard tracks:

- Turn time from acceptance to delivery, by property type and geography

- Revision request rate, by revision type

- UAD and GSE compliance error rates

- Lender-specific feedback and satisfaction signals

- Availability and capacity patterns over time

When this data is structured and continuously updated, automated routing systems can make assignment decisions that a human coordinator reviewing a static panel list physically cannot replicate. The system knows which appraiser has the lowest revision rate for complex rural properties in a specific county. The coordinator doesn’t, unless they’ve spent hours building that knowledge manually.

Automated systems that score appraiser performance based on turn time and revision rates, mapping coverage areas geographically to identify gaps, allow AMCs to manage panels of 100 or more appraisers without dedicated administrative staff. Scale that capability with AI-driven scoring models, and the panel management function becomes largely self-operating. Appraisal Host

This is why Go Source Valuations appraiser scorecard solutions are built not just as reporting tools, but as operational data infrastructure, the foundation that makes intelligent automation possible.

The Outsourcing Question: Build, Buy, or Partner?

For AMC operators evaluating how to build toward a dark back-office model, the strategic question isn’t just which workflows to automate; it’s how to resource the transition.

Three paths exist:

Build internally. AMCs with strong technology teams can develop proprietary automation systems tailored to their specific workflows. This offers maximum control but requires significant investment in development, maintenance, and ongoing AI model training.

Buy platform solutions. AMC software platforms are rapidly adding agentic automation capabilities. The risk: off-the-shelf solutions may not accommodate the specific lender requirements, quality standards, or workflow nuances that differentiate a given AMC’s operations.

Partner with specialized operational support providers. The most pragmatic path for most AMCs is to layer intelligent outsourced operational support over their existing technology stack. This approach captures the efficiency benefits of automation-enhanced operations without the capital investment of building proprietary systems and without the rigidity of pure platform dependency.

Businesses that combine AI, workflow automation, no-code platforms, integrations, governance, and human oversight will be better positioned to reduce manual effort, improve speed, control costs, and scale automation safely. For AMCs, that combination rarely comes from a single vendor; it comes from a deliberate operational architecture.

The Compliance Layer That Cannot Be Automated Away

One important constraint on the dark AMC model: regulatory compliance requires human accountability that AI cannot legally substitute.

AIR requirements mandate that AMCs maintain independence from lender influence in appraiser selection. That independence must be demonstrable and auditable. While agentic systems can enforce AIR-compliant rotation logic automatically, the accountability for that compliance remains with the AMC’s human leadership.

Similarly, USPAP compliance review involves professional judgment about appraisal methodology that goes beyond pattern matching. AI can flag common errors efficiently; only a qualified reviewer can evaluate whether an appraiser reasoning is sound.

The dark back-office model doesn’t eliminate these human functions; it concentrates human expertise on them, by automating the surrounding coordination noise that currently dilutes the attention of quality review staff.

Where AMCs Should Start Building Toward This Model

The shift toward dark back-office operations doesn’t require a wholesale technology transformation. It starts with identifying the specific workflows where automation delivers the clearest ROI:

Phase 1: Automate credential monitoring and license tracking. Low risk, immediate compliance benefit.

Phase 2: Implement performance-weighted appraiser scoring and integrate it into assignment logic. This is where operational quality gains compound over time.

Phase 3: Deploy AI-assisted quality flagging on incoming reports, reducing the volume of full manual reviews required.

Phase 4: Build automated lender communication workflows around SLA monitoring.

AMCs that execute these phases systematically over 18–24 months will find themselves operating at a fundamentally different efficiency level than competitors still running coordinator-heavy manual workflows.

The lights don’t have to go off at all at once. But the direction the industry is moving is clear.

FAQ: AMC Back-Office Automation

Q: Does back-office automation require replacing existing AMC software?

Not necessarily. Many automation capabilities can be layered on top of existing platforms through API integrations and specialized operational support. Complete platform replacement is rarely the right starting point.

Q: How does automated appraiser panel management maintain AIR compliance?

Properly designed automation enforces AIR-compliant rotation logic by removing any lender-specific preferencing from assignment decisions. The system assigns based on objective performance criteria, geography, and availability, which is exactly what AIR requires.

Q: What’s the ROI timeline for AMC back-office automation investments?

Credential monitoring and assignment automation typically deliver measurable efficiency gains within 60–90 days of implementation. Quality flagging and lender communication automation show ROI over a 6–12-month horizon as revision rates and SLA compliance metrics improves.

Q: Can smaller AMCs afford to build toward this model?

Yes, especially through outsourced operational partnerships, which provide access to automation-enhanced support without the capital investment of building proprietary systems. The dark back office is not exclusively a large-AMC advantage.