Your appraiser panel is one of the most regulated and most undermanaged assets in your entire AMC operation. Most AMC operators know they need a panel. Far fewer have the systems in place to manage it in a way that protects them during a lender audit or a state regulatory examination.

In 2026, that gap has become a serious business risk. Lenders are conducting due to diligence. State regulators are scrutinizing AMC panel documentation more closely. And the compliance standards that govern how you select, onboard, monitor, and remove appraisers from your panel have never been more specific or more enforceable.

This blog breaks down the compliance requirements that govern AMC appraiser panel management, the most common gaps that put AMCs at risk, and what a defensible panel management process looks like in practice.

Why AMC Appraiser Panel Management Is a Compliance Function, Not Just an Operations Function

Many AMCs treat panel management as a logistics problem, making sure you have enough appraisers to cover your order volume in every geography you serve. That’s necessary, but it’s not sufficient.

Under Dodd-Frank and the implementing regulations at 12 CFR Part 34 Subpart H, AMCs have specific obligations related to appraiser selection. They must ensure that appraisers on their panels hold current, valid state licenses or certifications in the state where the property is located. They must not select appraisers based on the value they are likely to provide. And they must maintain documentation demonstrating that their selection process is independent, consistent, and compliant with AIR requirements.

Beyond the federal floor, individual state AMC regulations add additional requirements. Some states mandate specific disclosure of language in appraiser engagement letters. Others require documented customary and reasonable (C&R) fee justification. Several require AMCs to maintain records of panel management decisions, including removals for a defined period.

The operational implication is significant: appraiser panel management is a compliance function that generates audit exposure if handled poorly. And most AMCs are handling it poorly.

The Most Common Panel Management Compliance Gaps

Based on what lenders and state regulators most frequently flag during AMC audits and due diligence reviews, these are the most common panel management failures:

Stale License and Certification Data: Appraiser licenses expire. E&O insurance policies lapse. An AMC that assigns an order to an appraiser whose license has expired, even by a few days, has a USPAP compliance problem and a potential lender of liability. Many AMCs are still checking license status manually and infrequently, which creates exposure windows.

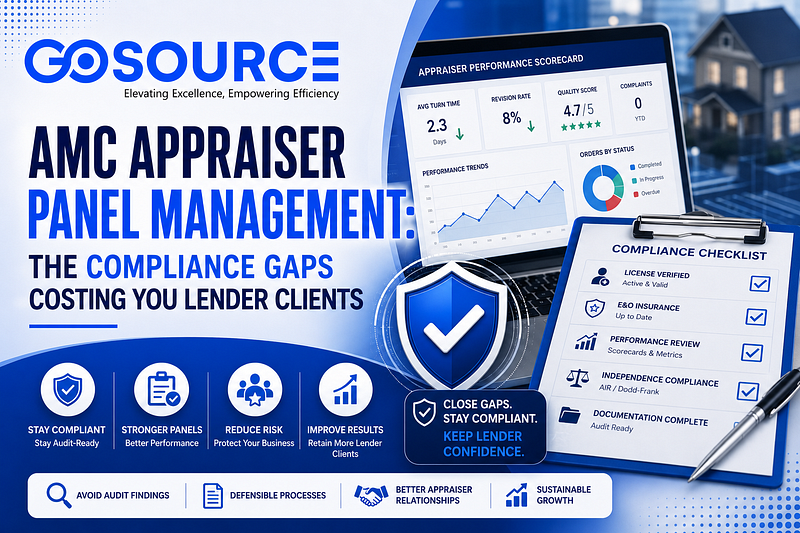

No Documented Performance Criteria: Selecting appraisers based on availability and geography is not enough. A defensible panel management process requires documented performance criteria: turnaround time metrics, revision rates, step rates, quality scores, complaint history. Without these, an AMC cannot demonstrate to a lender or regulator that its appraiser selection process is systematic and objective.

Inconsistent Onboarding Documentation: Many AMCs have appraiser onboarding processes that are inconsistent across staff members or markets. Some appraisers in the panel have completed files; others are missing executed engagement agreements, current E&O certificates, or license copies. This inconsistency is exactly what auditors are looking for.

No Formal Removal Process: AMCs often remove appraisers from their panels informally a conversation, a note in a spreadsheet, an email that never gets filed. A compliant panel management process requires documented removal procedures, including the reason for removal, the date, and any associated communication. Lenders increasingly ask for this documentation during vendor audits.

Geographic Coverage Gaps Without Documentation. When a lender requests an appraisal in a geography where your panel is thin, the temptation is to assign anyone available rather than document that coverage is limited and explain how you’re addressing it. Undisclosed coverage gaps create both quality risk and compliance risk.

What a Defensible AMC Panel Management Process Looks Like

A panel management process that can withstand a lender audit or state regulatory review has several core components:

Automated License Verification: License and certification status should be verified against state regulatory databases onboarding and regularly, not just when an order is assigned. E&O insurance should be tracked with expiration date alerts.

Documented Performance Scorecards: Each appraiser on the panel should have a performance scorecard that tracks key metrics over time: average turn time, revision request rate, quality score (if your QC process generates one), client complaint history, and any USPAP compliance issues. This scorecard is both a management tool and an audit defense.

Standardized Onboarding Packets: Every appraiser on the panel should have an identical set of onboarding documents: executed independent contractor or engagement agreement, current E&O certificate, license copy, geographic coverage confirmation, and any lender-specific credentialing requirements. These should be stored in a retrievable format not scattered across email threads.

Formal Removal and Suspension Protocols: Panel removals should follow a documented process: documented trigger (performance failure, license lapse, client complaint, ethical concern), notification to the appraiser, internal record of the decision and date, and file retention for the required period. Informal removals create legal and compliance exposure.

Rotation and Independence Compliance: AIR requires that AMCs not allow loan production staff to influence appraiser selection. Your panel management process should include documented rotation or selection criteria that demonstrate independence from loan production. This is an area of increasing regulatory scrutiny.

Geographic Coverage Mapping: You should be able to produce, on demand, a map or report showing your active panel coverage by state and county. Coverage gaps should be documented, along with your process for managing orders in underserved geographies.

The Lender Due Diligence Reality

Lenders, particularly bank lenders and those operating under OCC or CFPB oversight, are conducting more rigorous AMC vendors due to diligence than they were three years ago. The questionnaires are longer. The documentation requests are more specific. And the threshold for acceptable panel management practices has risen.

AMCs that cannot produce clean panel documentation, performance scorecards, and documented selection and removal procedures are losing lender clients to competitors who can. This is not a theoretical risk. It is a documented pattern in the current market.

The AMCs winning new lender business in 2026 are the ones that can demonstrate operational maturity and panel management documentation is one of the clearest signals of that maturity.

What an Outsourced Panel Management Support Changes the Equation

For AMCs that recognize their panel management process has gaps but lack the internal capacity to fix them, outsourced panel management support offers a practical path forward.

An experienced outsourcing partner can implement and maintain a structured panel management workflow, license verification, scorecard tracking, onboarding documentation, geographic coverage mapping, and removal documentation without requiring the AMC to hire additional full-time staff.

This is particularly valuable for mid-size AMCs operating in multiple states, where the volume and complexity of panel management tasks exceed what a single internal coordinator can handle effectively.

Go Source Valuation specializes in appraiser panel management support for AMCs, including performance scorecard systems, onboarding documentation, and license tracking workflows built to withstand lender and regulatory scrutiny. Learn more at gosourceval.com/appraiser-scorecard/.

FAQ Section

Q: What are the federal requirements for AMC appraiser panel management?

A: Under 12 CFR Part 34 Subpart H (implementing Title XI of FIRREA as amended by Dodd-Frank), AMCs must ensure that appraisers on their panels hold current, valid state credentials in the relevant jurisdiction and that appraiser selection is independent of loan production. Additional state-level requirements vary by jurisdiction.

Q: How often should AMCs verify appraiser license status?

A: At a minimum, license status should be verified at onboarding and at each order assignment. Best practice is automated, recurring verification against state regulatory databases at least quarterly, with real-time alerts for license lapses or E&O insurance expiration.

Q: What should be in an appraiser’s performance scorecard?

A: A compliant AMC appraiser scorecard typically tracks turn time performance, revision and step rates, client complaint history, quality control scores (where applicable), license status, and any documented USPAP compliance concerns. It should be updated regularly and retained in the appraiser panel file.

Q: Can an AMC remove an appraiser from its panel without documentation?

A: Technically, yes, but doing so creates compliance and legal exposure. A formal removal process with documented reasons, notification of records, and file retention is considered best practice and is increasingly required by lender-vendor management standards.

Q: How does outsourced panel management support work in practice?

A: An outsourced panel management partner implements and maintains the AMC’s panel workflows, license tracking, scorecard updating, and onboarding documentation and geographic coverage mapping on behalf of the AMC, integrating with existing systems and delivering clean, audit-ready records.