Mortgage lenders talk a lot about rate competitiveness, processing speed, and borrower experience. But one variable consistently escapes that conversation appraisal of turn time.

The time between the appraisal order and the delivered report can make or break a closing timeline. Yet many lenders treat it as an acceptable unknown, something that happens on the AMC’s side of the wall that they can’t really control. That mindset is costing them loans.

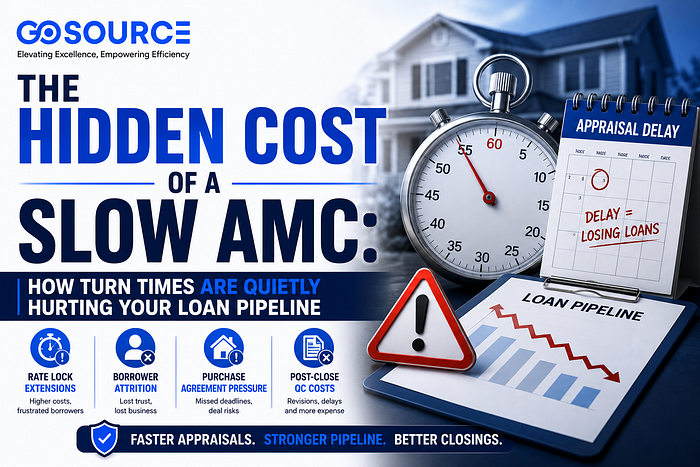

What Turn Time Actually Affects

Appraisal turn time doesn’t exist in isolation. It sits at the center of a chain of downstream decisions and costs that most lenders underestimate until something goes wrong.

Rate Lock Extensions

When an appraisal runs behind schedule, lenders often face rate lock extension requests, and those extensions aren’t free. Depending on the lender rate lock policy and current rate environment, an extension can cost the borrower anywhere from a small fee to a meaningful rate of adjustment. Either way, it introduces friction at exactly the wrong moment in the borrower’s relationship.

Borrower Attrition

A delayed appraisal is often the moment a borrower starts questioning whether they made the right lender choice. In purchase markets, especially, buyers are anxious. Sellers are watching timelines. A lender who can’t give a clear answer on when the appraisal will be completed signals operational disorganization. Some borrowers walk. Others are close, but they don’t refer to them.

Purchase Agreement Pressure

In competitive purchase markets, delayed appraisals can push closing dates past contractual deadlines. This puts lenders in the position of negotiating extensions with sellers, a conversation that can unravel deals, particularly in markets where seller leverage is high.

Post-Close QC Costs

Here’s a less obvious one: rushed appraisals that are completed under time pressure often have higher rates of QC failures. When an AMC is scrambling to meet a deadline, appraiser assignment decisions may prioritize availability over competency. The result is reports that need revision, further delaying the process, and adding post-close correction costs.

Why Turn Time Problems Usually Start at the AMC Level

Lenders sometimes assume appraisal delays are driven by market conditions, appraiser availability, geographic challenges, and complex property types. And those factors are real. But a significant portion of turn-time variance across lenders using the same markets is attributable to the AMC’s internal operations, not external conditions.

The AMC is responsible for:

- Receiving the order and initiating the assignment

- Matching the order to a qualified appraiser based on geography, license, and property type competency

- Communicating the assignment and confirming acceptance

- Following up during inspection scheduling

- Receiving and reviewing the completed report

- Conducting a quality control review before delivery

- Delivering the final report to the lender

Each of these steps has an internal cycle time. An AMC with a strong operational infrastructure moves through this chain efficiently. An AMC with understaffed coordination teams, manual workflows, or weak QC processes accumulates delays at every handoff.

The lender often doesn’t see where the delay is occurring. They just see that the report is late.

The Geography Problem AMCs Don’t Discuss Enough

One of the least-discussed drivers of appraisal delays is panel depth, specifically, how well an AMC’s appraiser panel is populated in the markets you lend in.

Large AMCs often advertise national coverage, and technically, that’s accurate. But coverage and density are different things. In suburban markets with high order volume, an AMC might have excellent panel depth, multiple qualified appraisers available for quick assignment, and quick inspection scheduling.

In rural markets, secondary markets, or specialty property types, the same AMC might have one or two panel appraisers, and if both are busy, orders queue. The lender sees a delay. The real cause is panel depth, and that’s a question lender should ask prospectively, not reactively.

Before assigning appraisal orders in a new market, ask your AMC: how many active, credentialed appraisers do you have in this county? What is your average assignment acceptance rate in this market? What’s your historical turn time for this geography?

If an AMC can’t answer those questions from data, that’s a signal.

What High-Performing AMC Relationships Look Like

Lenders who consistently achieve faster, cleaner appraisal cycles share a few common characteristics in how they manage their AMC relationships.

Clear Performance Expectations in Writing

Lenders with strong AMC relationships have defined turn-time standards in their vendor contracts, not just aspirational language but specific commitments by market type. Urban markets, suburban markets, and rural markets have different expected cycle times. Those differences should be reflected in the agreement.

Regular Performance Data Reviews

Turn time should be a standing agenda item in any AMC vendor review. Lenders should be pulling monthly data on average cycle time by market, order type, and appraiser. If the AMC can’t provide that data in a structured format, that’s a gap in their operational visibility and yours.

Escalation Pathways That Actually Work

When an order is at risk of missing a rate lock deadline, who do you call? If the answer is “a general inbox,” you don’t have a real escalation pathway. Strong AMC relationships include named account contacts with actual authority to expedite and communicate, not call center routing.

QC That Happens Before Delivery

Turn time and quality are not opposing forces. The fastest AMC deliveries that still require post-close corrections don’t save lenders on anything; they just move the delay further downstream. The best AMC partners have quality control integrated into the delivery cycle, so lenders receive reports that are ready for underwriting review, not reports that require revision requests.

The Case for Outsourced AMC Operations Support

Some lenders are taking a different approach: rather than trying to optimize their relationship with a single AMC or manage multiple AMC vendors internally, they’re working with outsourced AMC operations partners who sit behind the scenes to coordinate, review, and manage the appraisal cycle on the lender’s behalf.

This model doesn’t replace the AMC. It adds a layer of dedicated operational support between the lender and the AMC, handling order tracking, QC review, escalation management, and performance reporting. For lenders processing meaningful appraisal volume, this operational layer can meaningfully reduce turn times, improve report quality, and free up internal staff to focus on loan production.

The key is finding an operations support partner with genuine appraisal industry expertise not a generic outsourcing firm, but a team that understands USPAP, QC review criteria, and AMC workflows from the inside.

A Turn-Time Audit Worth Running

Pull your last 90 days of appraisal data and look for these patterns:

- What are your average days from order to delivery across your top three markets?

- What percentage of orders exceeded your target turn time?

- How many orders require post-close revision requests?

- How many rate lock extensions were directly attributable to appraisal delay?

- What is your UCDP first submission acceptance rate?

If you haven’t looked at these numbers recently, the answers might be uncomfortable. But they’re also actionable. Turn time is not just an AMC problem; it’s a lender pipeline problem, and it’s one of the few variables in the mortgage process where targeted operational changes produce fast, measurable results.

Your closing timeline is only as strong as its slowest step. For too many lenders, that step is still appraisal.

FAQ

Q: What’s a reasonable appraisal turn time for urban vs. rural markets?

In well-covered urban and suburban markets, 5–7 business days from order to delivery are achievable. Rural and specialty markets typically run 10–15 business days, sometimes longer in areas with a thin appraiser panel depth.

Q: Can lenders negotiate turn-time commitments directly with AMCs?

Yes, and they should. Turn-time expectations by market type should be documented in vendor agreements. AMCs that resist committing to specific performance standards should be treated as a vendor risk flag.

Q: What causes UCDP submission failures, and how does an AMC affect them?

UCDP failures are typically caused by data entry errors, methodology inconsistencies, or missing required fields. AMCs with robust QC processes catch these before submission. Low first-submission acceptance rates are a reliable indicator of weak AMC quality control.

Q: Is outsourced appraisal operations support the same as using a second AMC?

No. An outsourced operations partner doesn’t manage appraiser panels or hold AMC licensing. They provide coordination, quality review, and escalation support on the lender’s behalf — working with your existing AMC relationships rather than replacing them.