How Lenders and AMCs Can Build an ROV Process That’s Compliant, Efficient, and Dispute-Proof

The Reconsideration of Value has been part of the mortgage appraisal ecosystem for decades, but 2024 changed everything. New federal guidelines issued by a coalition of banking regulators transformed the ROV from an informal, inconsistently applied process into a formal compliance obligation, one with documentation requirements, response timelines, and anti-coercion provisions that carry real regulatory risk if ignored.

For lenders and appraisal management companies, the question is no longer whether to have an ROV process. The question is whether the one you have is actually compliant and whether it can scale without creating operational chaos.

This article breaks down what the updated rules require, where most ROV workflows break down, and how to build a process that protects your institution, serves your borrowers, and supports your appraiser relationships.

Why the 2024 ROV Rule Changes Matter for Your Operations

Before diving into process design, it’s worth understanding the regulatory context driving these changes.

In August 2024, six federal agencies in the OCC, FDIC, Federal Reserve Board, NCUA, CFPB, and FHFA finalized guidance requiring lenders to adopt formal ROV policies. The impetus was a growing body of research showing that appraisal bias, particularly in communities of color, had been systematically undervaluing homes with limited recourse for affected borrowers.

The practical effect on lending operations includes:

- Written policy requirement: Every covered institution must have a documented ROV policy that describes the process borrowers can use to challenge an appraisal

- Advance appraisal delivery: Borrowers must receive their appraisal report at least three business days before closing, giving them time to review and submit an ROV if warranted

- Structured response requirements: Appraisers must address each piece of evidence submitted in a properly formatted ROV request in writing

- Prohibition on improper influence: Policies must explicitly prohibit lender staff from pressuring appraisers to change values for reasons other than legitimate factual or methodological concerns

For AMCs that sit between lenders and appraisers, these rules create layered obligations. You’re responsible not just for routing ROV requests but for ensuring the appraisers on your panel understand how to respond to them compliantly and that your documentation systems can produce a clean audit trail if a regulator asks to see it.

The Go Source Valuation team has published a practical breakdown of what these ROV requirements mean for lenders and appraisers including the eight operational steps that make the process defensible.

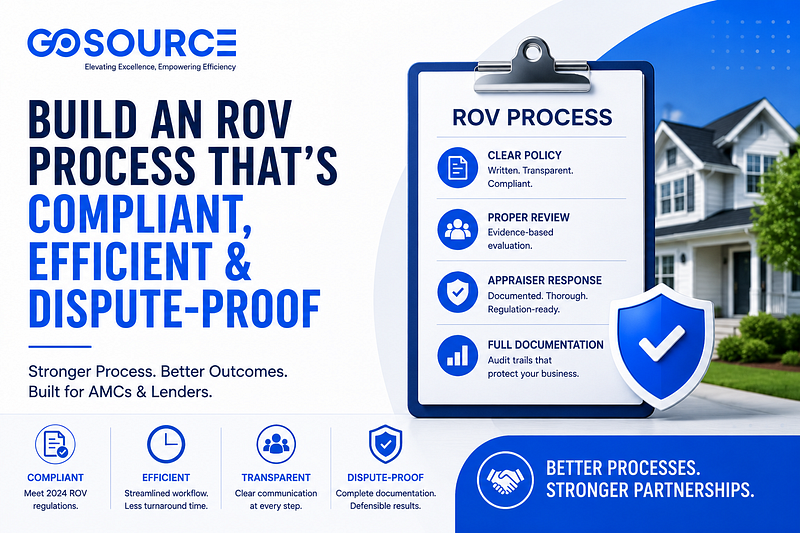

The Four Stages of a Compliant ROV Workflow

A well-designed ROV process moves through four distinct stages. Each stage has specific inputs, outputs, and compliance checkpoints.

Stage 1: Request Receipt and Triage

The workflow begins the moment a borrower (or their agent) submits an ROV request through your institution. At this stage, you need to:

- Acknowledge receipt in writing within one business day

- Log the request in your loan management or appraisal management system with a timestamp

- Assign a point of contact for the borrower

- Conduct an initial triage to confirm the request includes evidence (not just a statement of dissatisfaction)

This triage step is important. Many ROV requests arrive without supporting documentation — just a claim that the value is wrong. While you’re generally obligated to forward a properly formatted request to the appraiser, forwarding an unsupported complaint creates problems for everyone. Your policy should define what a “complete” ROV request looks like, so you can request additional documentation before routing it.

Stage 2: Evidence Review and Routing

Once you have a complete request, the evidence needs to be reviewed before it reaches the appraiser. This doesn’t mean evaluating whether the comparables are better — that’s the appraiser’s job. It means confirming that the submission is coherent, contains identifiable comparable sales or documented factual claims, and doesn’t include anything that would constitute inappropriate influence.

Appraisers cannot be told “the buyer wants $X” or “the deal falls apart below $Y.” Evidence packets must be scrubbed to remove purchase price references, contract terms, and any language that could be read as pressure to hit a number. This is a compliance-critical step that needs to happen at the institution level, not on the appraiser’s desk.

Once scrubbed, the packet goes to the original appraiser (or the AMC’s review desk, if the original appraiser is unavailable or has a conflict).

Stage 3: Appraiser Analysis and Response

The appraiser now has the most important role in the process. Under the updated guidelines, they’re required to:

- Review each comparable sale or factual correction submitted

- Document whether they agree or disagree with each item and why

- If the evidence warrants a value change, provide a revised report or addendum

- If the evidence doesn’t support a change, explain their reasoning in writing

This is where many existing ROV processes fall short. Appraisers who haven’t been trained on the new requirements often write dismissive one-line responses (“comparable reviewed, not applicable”) or don’t address submitted evidence at all. That’s not compliant under the new framework, and it creates audit risk for the lender.

AMCs play a critical quality control role here. Before the appraiser’s ROV response goes back to the lender or borrower, it should be reviewed to ensure each piece of evidence was addressed substantively. This is also where appraiser scorecard data becomes valuable if certain appraisers on your panel have a pattern of nonresponsive ROV handling; that’s a performance flag that needs to be addressed.

Stage 4: Determination and Documentation

The final stage is closing the loop. The borrower needs to receive:

- A written summary of the appraiser’s response to each item in the ROV

- A clear statement of the final value determination

- Information about next steps if the value was not revised

Documentation from all four stages should be retained in the loan file. If a fair lending complaint or regulatory examination later raises questions about how an ROV was handled, you need a complete, timestamped paper trail showing that the process was followed correctly.

Common ROV Workflow Failures and How to Fix Them

Even well-intentioned institutions make predictable mistakes in ROV handling. Here are the most common failures and the fixes:

Failure: No written policy exists

Fix: Document your ROV policy now. It doesn’t need to be elaborate, but it needs to exist, be accessible to borrowers, and describe the process clearly. Include timelines, evidence requirements, and escalation paths.

Failure: ROV requests go directly to the appraiser from the borrower

Fix: All ROV communication must be routed through the lender. Direct contact between borrowers and appraisers creates an appraiser independence problem and potentially a fair lending issue. Your intake process should capture all requests at the level of lender.

Failure: Evidence packets aren’t scrubbed before going to the appraiser

Fix: Assign someone, ideally a compliance-trained member of your appraisal operations team, to review all evidence submissions before they leave your institution. The purchase price, contract terms, and anything that could be read as pressure must be removed.

Failure: Appraisers aren’t trained on ROV response requirements

Fix: If you manage an appraiser panel, make ROV response training part of your onboarding and annual compliance review process. Appraisers need to know exactly what a compliant written response looks like.

Failure: Response timelines are undefined

Fix: Set specific internal timelines and hold them. An ROV request that sits in someone’s inbox for three weeks creates borrower complaints, pipeline delays, and regulatory exposure. Most institutions target five to seven business days for a complete cycle.

Failure: Documentation is incomplete or inconsistently maintained

Fix: Build ROV documentation into your standard loan file checklist. Every stage receipt, evidence review, appraiser response, and final determination should generate a timestamped record.

The Technology Layer: What Your Systems Need to Support

Modern ROV compliance is difficult to achieve with manual, email-based workflows, especially at scale. Institutions originating significant loan volume need technology infrastructure that can:

- Track ROV requests from intake to resolution with timestamps at each stage

- Maintain a searchable audit log of all communications and evidence packets

- Flag response timeline breaches before they create compliance problems

- Generate summary reports for fair lending analysis and regulatory examinations

- Support appraiser panel performance tracking including ROV response quality

Appraisal management software platforms have increasingly built ROV workflow modules into their core functionality. If your current system doesn’t support this, that’s a gap worth addressing, particularly as regulators begin conducting examinations specifically focused on ROV compliance.

For appraisers and AMCs looking to tighten their operational workflows around ROV and related compliance requirements, understanding what an efficient, defensible process looks like at the operational level is the starting point. GoSource Valuation’s reconsideration of value resource outlines the key steps and considerations that apply across the lifecycle of a compliant ROV request.

Training Your Team: Who Needs to Know What

ROV compliance isn’t just an appraisal of operations issues. Multiple teams within a lending institution touch the process, and each needs appropriate training.

Loan Officers and Processors

They’re often the first point of contact when a borrower is upset about an appraisal. They need to know:

- What an ROV is and how to explain it to borrowers without overpromising outcomes

- How to receive and log ROV requests

- What a “complete” request looks like and how to guide borrowers in assembling one

- What they are absolutely prohibited from saying to appraisers

Appraisal Desk / AMC Operations Staff

They manage the actual routing of ROV requests and need to know:

- How to conduct evidence review and scrubbing

- Internal routing timelines and escalation procedures

- How to evaluate whether an appraiser’s response was substantively compliant

Compliance and Legal

They need to understand the regulatory framework well enough to:

- Review and approve your written ROV policy

- Conduct periodic audits of ROV documentation

- Respond to borrower complaints and regulatory inquiries related to ROV outcomes

Executive Leadership

They need to understand that ROV compliance is not optional and that regulatory examinations are increasingly focused on this area. Fair lending analysis increasingly incorporates appraisal data, and institutions without defensible ROV processes face elevated examination risk.

ROV and Fair Lending: The Connection You Can’t Ignore

One of the core drivers of the 2024 regulatory changes was the documented relationship between appraisal outcomes and race. Studies, including research by the Brookings Institution and analyses commissioned by the FHFA, found that homes in predominantly Black and Hispanic neighborhoods were more frequently appraised below contract price and received lower values than comparable homes in predominantly white neighborhoods.

The new ROV framework was designed in part to give affected borrowers a formal, documented way to challenge potentially biased appraisals. For lenders, this creates an important fair lending obligation: your ROV outcomes need to be monitored for disparate impact.

If analysis of your ROV data shows that requests from borrowers in protected classes are being denied at higher rates or that appraiser responses to ROV requests from minority borrowers are less thorough, that’s a fair lending flag that regulators will notice before you do.

Build fair lending monitoring into your ROV reporting from the start. Track:

- ROV request rates by geography and borrower demographics

- ROV approval/denial rates by demographic segment

- Appraiser response quality metrics by geography

- Time-to-resolution broken out by loan type and geography

This data won’t just protect you in examinations; it will also reveal whether your appraisal process is working equitably, which is ultimately the point.

Building Appraiser Relationships That Support ROV Compliance

The final piece of a sustainable ROV operation is the appraiser relationship. ROV requests, when handled poorly, damage trust between lenders, AMCs, and appraisers. When handled well, they actually strengthen it.

Appraisers want to produce accurate appraisals. When an ROV surfaces a genuine error or a missed comparable, most appraisers will correct it willingly. The ROV process only creates friction when:

- It’s used as a pressure tool to hit a number (which the new rules explicitly prohibit)

- Evidence packets are incomplete or contain inappropriate language

- Appraisers aren’t given enough time to respond thoughtfully

- Their compliant responses are not acknowledged or communicated clearly

If you’re an AMC, your appraiser panel management strategy should explicitly address ROV handling. Appraisers who respond compliantly, thoroughly, and on time to ROV requests should be recognized. Those who don’t receive training and, if the pattern continues, performance consequences.

A well-functioning ROV process, one where appraisers feel respected and the evidence standard is clear results in more accurate appraisals over time, fewer disputes, and faster loan closings.

Frequently Asked Questions: ROV Compliance for Lenders and AMCs

Q: Are all lenders required to have a written ROV policy under the 2024 rules?

Yes. The interagency guidance issued in 2024 requires all covered institutions to maintain a written policy governing the ROV process. This includes large banks, community banks, credit unions, and non-bank mortgage lenders subject to federal oversight.

Q: Does the ROV requirement apply to every loan type?

The interagency guidance applies broadly to residential mortgage transactions. Fannie Mae and Freddie Mac have their own seller/servicer requirements that may vary slightly in their specifics. Always check current GSE guidelines in addition to the interagency framework.

Q: How quickly must we respond to a borrower’s ROV request?

The regulations don’t set up a single universal timeline, but they require that lenders process ROV requests in a manner that doesn’t unnecessarily delay the loan transaction. Most compliance guidance recommends a five to seven business day target for complete cycle time.

Q: What if an appraiser refuses to address the evidence in an ROV?

This is a compliance and panel management issue. The appraiser engagement letter and your AMC agreement should specify ROV response requirements. If an appraiser consistently fails to provide substantive written responses, that’s grounded for removing them from your approved panel.

Q: Can we order a second appraisal instead of processing an ROV?

A second appraisal may be appropriate in some circumstances, particularly when there’s evidence of appraiser bias or a fundamental methodological error. However, it should not be used as a substitute for a properly processed ROV or to simply shop for a higher value. The decision to order a second appraisal should be documented and justified.

Q: How should we handle ROV requests that don’t include any supporting evidence?

Your written policy should define what a “complete” ROV request looks like. If a submission doesn’t include any evidence, just a statement that the borrower thinks the value is wrong, you can (and should) notify the borrower in writing that additional documentation is needed before the request can be routed to the appraiser.

Q: Are we required to tell the borrower why their ROV was denied?

Under the updated guidelines, borrowers should receive a written explanation of the appraiser’s response to each item of evidence they submitted. That explanation, in aggregate, constitutes the rationale for the outcome. A simple “denied” with no explanation is not compliant.

Q: What documentation should we retain and for how long?

All documentation related to the ROV the original request, evidence packets, appraiser responses, communications, and final determination should be retained as part of the loan file for at least the period required by your federal regulator’s record retention rules. For most institutions, that’s a minimum of three years after the final disposition of the loan.

Q: How does ROV compliance intersect with ECOA and fair lending?

ROV outcomes are increasingly being analyzed in HMDA and fair lending examinations. Disparate patterns in ROV denial rates by race, ethnicity, or national origin can be a fair lending practice flag. Your compliance program should include periodic analysis of ROV outcome data disaggregated by demographic variables.

Q: Where can we find operational guidance on building a compliant ROV workflow?

The interagency guidance document is the primary regulatory source. For practical, operational guidance on what a compliant eight-step ROV process looks like in practice, GoSource Valuation’s reconsideration of value page is a useful industry resource with a practitioner-focused perspective.

Final Thoughts

The Reconsideration of Value process is no longer something lenders and AMCs can handle ad hoc. The 2024 regulatory changes elevated it to a formal compliance function — one with documentation requirements, timeline obligations, anti-coercion provisions, and fair lending implications.

The institutions that will navigate this well are those that build the process deliberately: clear written policies, trained staff, technology-supported workflows, strong appraiser relationships, and ongoing data monitoring.

The goal, ultimately, is the same one an appraiser has always had: accuracy. A well-run ROV process doesn’t undermine appraisal integrity; it strengthens it by creating a structured, documented way to catch and correct the errors that inevitably occur in any high-volume valuation operation.

Build the process right, and ROVs stop being a source of stress and start being evidence that your quality control is working.