The mortgage lending process has never been simple. Between coordinating appraisers, meeting compliance deadlines, managing documentation, and communicating with borrowers, the operational load on lending teams is substantial. And in a rate-sensitive market where loan cycle speed directly affects competitive position, one bottleneck in the appraisal workflow can cost a lender real business.

That’s why a growing number of lenders from independent mortgage banks to large regional institutions are investing in appraisal management software. Not as a luxury, but as a core operational tool.

This article breaks down what appraisal management software does, why legacy manual processes are increasingly untenable, and what lenders should look for when evaluating a solution.

The Problem with Manual Appraisal Management

For years, many lenders managed appraisals the same way: a mix of spreadsheets, email chains, phone calls, and internal checklists. The process worked barely when loan volumes were manageable, and regulatory requirements were less demanding.

Today, neither of those conditions holds.

Loan volumes fluctuate sharply with rate cycles. Compliance requirements under Dodd-Frank, USPAP, and GSE guidelines have grown more rigorous. The rise of hybrid and desktop appraisals under UAD 3.6 is introducing new workflow complexity. And borrower expectations around turnaround time have tightened considerably.

Manual processes crack under this pressure. Appraisers get assigned to the wrong geography. Deadlines slip because no one is tracking real-time order status. Fee disputes arise from unclear records. Audit trails are incomplete or inconsistent.

These aren’t just operational inconveniences of their compliance liabilities.

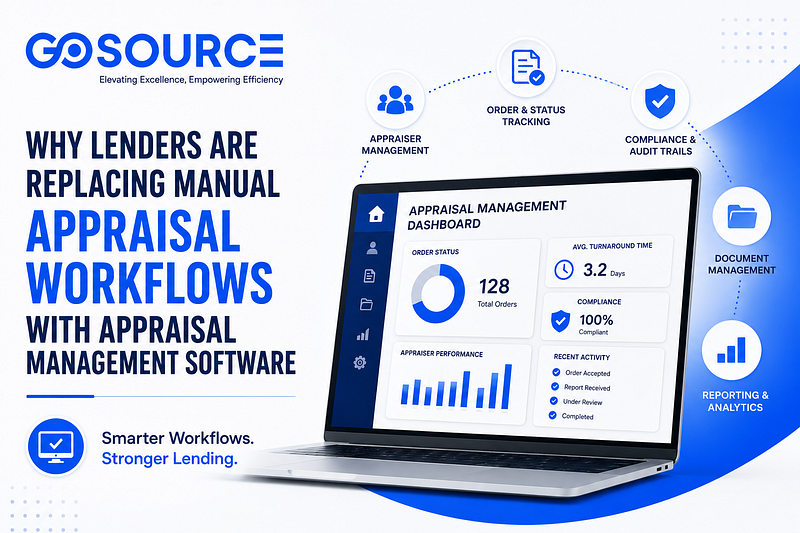

What Appraisal Management Software Actually Does

Appraisal management software is a purpose-built platform that centralizes and automates the end-to-end appraisal workflow. Rather than managing appraisal orders across email, phone, and disconnected systems, everything lives in one place: order placement, appraiser assignment, status tracking, document storage, compliance monitoring, and reporting.

Here’s what that looks like in practice:

Appraiser Panel Management

The software maintains a searchable database of qualified appraisers, including credentials, geographic coverage, license status, and performance history. Assignment logic, whether manual or automated, draws this data to match the right appraiser to each order. This eliminates the guesswork and the risk of assigning a job to someone who isn’t qualified or licensed for that county.

Order Tracking and Status Visibility

Once an order is placed, lenders can see exactly where it stands in real time: accepted, in progress, under review, or complete. Automated notifications alert the right people at each stage, removing the need for manual follow-up calls and emails.

Compliance and Audit Trail Management

This is arguably the most critical function for lenders operating in regulated environments. Appraisal management software logs every action taken on every order assigned to it: when, what changes were made, when the report was received, and when it was reviewed. This creates a defensible audit trail that satisfies USPAP, Dodd-Frank independence requirements, and GSE guidelines.

Document Storage and Version Control

Appraisal reports, revision requests, inspection photos, and correspondence are stored digitally and linked to the order record. Version control ensures the team is always working from the most current document, and nothing gets lost in an email thread.

Fee and Cost Management

The software automatically calculates appraisal fees based on property type, complexity, and geography. Invoicing is generated upon completion, and cost tracking provides visibility into appraisal-related expenses across the portfolio.

Reporting and Performance Analytics

Lenders can pull data on average turnaround times, appraiser performance, order volume trends, and compliance metrics. This isn’t just useful for operations; it’s essential for quality control and vendor management.

To see how these capabilities come together in a fully managed appraisal workflow, GoSource Valuation’s appraisal management software overview is a strong reference for lenders evaluating the space.

The Compliance Case Is Particularly Strong

It’s worth pausing the compliance dimension, because it tends to be underweighted in discussions of appraisal technology.

Appraisal independence requirements under Dodd-Frank prohibit loan production staff from influencing the appraisal process. USPAP Standards govern how appraisals are conducted and reviewed. GSE eligibility requirements set specific documentation and process standards for conventional loan appraisals.

Manual workflows make compliance fragile. It’s hard to prove independence when communication happens over personal email. It’s hard to demonstrate USPAP adherence when there’s no systematic review record. It’s hard to satisfy a GSE audit when documentation is scattered across systems.

Appraisal management software builds compliance structurally through access controls, documented workflows, and audit logs that exist regardless of whether anyone remembered to create them manually. For lenders who’ve faced scrutiny on appraisal processes, this is a significant risk reduction.

Integration with the Broader Lending Stack

Modern appraisal management platforms don’t operate in isolation. The best ones integrate with loan origination systems (LOS) and CRM platforms, allowing appraisal data to flow into the loan file automatically rather than requiring manual data entry at handoff points.

This integration matters for two reasons. First, it reduces re-keying errors, one of the most common sources of delays and discrepancies in mortgage operations. Second, it gives loan officers real-time visibility into appraisal status from within the systems they already use, improving internal communication without adding another platform to monitor.

What Lenders Should Look for When Evaluating Software

Not all appraisal management software is built the same way. Some platforms are designed primarily for AMCs and bolt-on lender features as an afterthought. Others are consumer-facing origination tools that treat appraisal management as a secondary function.

Lenders evaluating options should prioritize the following:

Does the compliance architecture ensure that the system maintains defensible audit trails and enforces independence requirements by design? Appraiser panel flexibility: Can you manage your own preferred vendor panel, or are you locked into the platform network? Reporting depth, can you surface the performance data you actually need for QC and vendor management? LOS integration: How clean is the connection to your existing loan origination workflow? Support the model when something breaks into a high-volume environment. How quickly can you get a resolution?

For lenders who want managed support alongside software infrastructure rather than just a self-service platform, Go Source Valuation’s AMC operations services offer a hybrid model worth considering.

FAQ: Appraisal Management Software for Lenders

What is appraisal management software?

It’s a platform that centralizes and automates the appraisal workflow for mortgage lenders from ordering and appraiser assignment to status tracking, document management, compliance monitoring, and reporting.

Is appraisal management software only for large lenders?

No. Smaller independent mortgage banks and community lenders benefit significantly from appraisal software because they typically lack the internal staffing to manage high-volume appraisal operations manually. The efficiency gains are proportionally larger for leaner operations.

How does this software support USPAP compliance?

By maintaining complete audit trails, enforcing review workflows, and documenting every action taken on each appraisal order. This creates a defensible record of process adherence without relying on manual documentation practices.

Can appraisal management software handle hybrid and desktop appraisals?

Modern platforms are designed to accommodate evolving appraisal types, including hybrid and desktop appraisals introduced under UAD 3.6. The order management and document storage features adapt to different appraisal form types and inspection workflows.

What’s the difference between appraisal management software and an AMC?

An AMC (appraisal management company) is a third-party organization that manages the appraisal process on a lender’s behalf. Appraisal management software is a technology platform. Some lenders use software to manage their own appraiser panels in-house; others engage AMCs that use the same type of software operationally.

How long does implementation typically take?

This varies by vendor and lender complexity, but most platforms can be operationalized in a matter of weeks. LOS integration is usually the longest-lead item.

The Bottom Line

Appraisal management software isn’t a nice-to-have for lenders who handle meaningful appraisal volume; its foundational infrastructure. The compliance exposure from manual workflows, the operational drag on turnaround times, and the data blind spots in appraiser management all represent costs that accumulate quietly until they become acute.

For lenders looking to build a faster, cleaner, and more defensible appraisal operation, the conversation starts with the right software and the right operational partner. For an in-depth look at what modern appraisal management infrastructure can offer, visit the GoSource Valuation resource library.