武藤さんは人気なさそうですねw ブルームバーグが発表するやいなや下げましたもんね。

但し、白川さんを追い込んだ安倍さんに期待というか、今更政府方針を変更できないと読む方が利にかなっています。

反応がどうでるか?来週にも結果が出てくるか?

野村証券恐ろしw

この記事のコメントで色々判断したい。

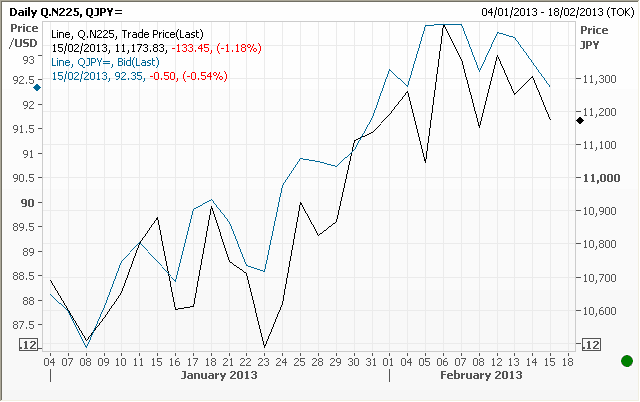

It’s the latest in Japanese swings and roundabouts, pushing the yen

higher and JGB yields and stocks lower… What to blame? What to blame?

Russian finance minister Anton Siluanov’s call for a G20 statement with more “specific” language opposing currency intervention may have had something to do with it.

This Reuters story that appeared a few hours ago on the new Bank of Japan governor also helped move things along:

“The choice of Muto appears to be gaining momentum,” said one of the sources familiar with the selection process.

That’s Toshiro Muto, who was actually the LDP’s original nominee for

BoJ governor back in 2008 when Yasuo Fukuda was prime minister (Fukuda

replaced Abe after the latter resigned in September 2007).

Back in December, Nomura analysts said Muto and fellow MoF-aligned

contender for the BoJ post, Eijiro Katsu, were “more reserved” about

monetary easing than their likely key rivals with academic backgrounds:

Mr Muto has said that numerous policy options are

available and although he is clearly more dovish than Mr Shirakawa, he

has not suggested anything more exotic than the BOJ’s current asset

purchasing programs. He is also somewhat negative about inflation

targeting, saying it would not necessarily be a good idea to raise the

target to 2% before achieving 1% inflation. He is also markedly negative

about the purchase of overseas bonds, which may reflect his MOF

background.

And they produced this handy cut out and keep chart earlier this month when current governor Shirakawa announced his intention to leave the job a few weeks early (in March):

Interesting because the BoJ has already gone a little further than Muto’s comments would suggest he is comfortable with, by announcing last

month a 2 per cent CPI target. And that actually didn’t impress too

many people for long, but the focus has been on the new BoJ governor (or

governors, as the two deputies’ terms also end next month) — and on the

apparent politicisation of monetary policy.

On Thursday afternoon, a WSJ report

said that Muto was one of two contenders; the other being Kazumasa

Iwata, “an academic known as an advocate for unconventional monetary

easing policy”. Indeed, Nomura noted

that Iwata was one of the four top contenders to have most openly

supported a 2 per cent inflation target, and that he “enthusiastically

in favor of overseas bond purchases by the BOJ”. Have a look back at

that table again and focus on the bottom line.

The WSJ story suggests that while prime minister Shinzo Abe prefer

Iwata, finance minister Taro Aso and many people within their government

and at the BoJ prefer Muto, in part because he has experience at both

the MoF and the BoJ:

“The next governor will face a very difficult task of

beating deflation but also maintain confidence in Japan’s fiscal policy.

That would require an ability to deal with politicians. I think Mr.

Muto would be great at that,” said a lawmaker with Mr. Abe’s ruling

Liberal Democratic Party.

Again, even if Muto is the next BoJ governor, who’s to say what he

will actually do in the post? The WSJ notes that his views have changed:

While Mr. Muto now advocates more easing action from the

BOJ, his critics note that during his time as deputy BOJ governor, he

didn’t oppose two instances where the bank tightened credit, a decision

blamed for prolonging deflation. But his supporters say such

“flexibility” to change positions is an asset.“He listens to others and adopts what he thinks is good at the time.

If he sees that reflation is the flavor of the day, he’ll go with it,

but he can adjust later. That’s convenient for politicians, too,” said a

finance ministry official who has worked with Mr. Muto.

Abenomics: it’s still all about the guesswork.

Additional reporting by David Keohane

Related links:

All’s fair in love and currency wars – FT Alphaville

Cut-out-and-keep guide to prospective BoJ governors – FT Alphaville

Abe Faces Rift Over BOJ Governor – WSJ

Moving targets and a lack of self-belief at the BoJ – FT Alphaville

This Japanese election may be different – Gavyn Davies’ blog

Report

fiatsceptic |

February 16 5:11am |

Permalink

The drama over the young government’s lapse in proper euphemism seems

over…..global CB linguistic plumage smoothed. They’ll describe their

debasement with more political correctness in the future. And the

needle has moved a bit toward competitive debasement.

Bill from Ohio: “We seem to be in a era which will result in either the

growth, or demolition of our assets by the fiats of politicians.” This

is a broad, important theme which, while certainly not absent in the FT,

deserves more analysis and a couple of spotlights.

Report

now what |

February 15 5:34pm |

Permalink

Mrs Lagarde was also playing down the severity of the economic crisis

Report

globalobserver |

February 15 2:52pm |

Permalink

Japan has been used (for far too long( by the USA and the Europeans

(including the UK) manipulating their currencies to the detriment of the

Japanese economy. It is surprising that the Japanese have taken 20

years to realise this!

Report

Apostle |

February 15 2:40pm |

Permalink

If our government prints trillions in money and spends it, weakening

the dollar, it is necessary economic stimulation. Media talk heads drool

over how it helps jobs, export, prudent avoidance of the cliff.

If Japanese government prints trillions in money and spends it, weakening the yen, it is improper fiscal policy.

Japan should do what is good for the long suffering Japanese people. Weaken the yen to above 100 per dollar.

Report

Bill from Ohio |

February 15 2:04pm |

Permalink

The battle of the Yen will be long and bloody.

Abe government has lowered its tone going into these meetings and the

last meeting of the Central Bank was held under it's outgoing

leadership. This is just a lull in the process.

The 20 year appreciation of the Yen will be reversed is some greater

manner, Japan's demographics and economy demand it. "Currency Wars"

like all others are fought from national necessity and will only be

halted when the nations interests suggest it. Diplomacy will not change

national interest.

Those of us with assets to protect and grow need to be using the dance

of these elephants to profit from the changing times. We seem to be in a

era which will result in either the growth, or demolition of our assets

by the fiats of politicians. These are time to be mercenaries in the

markets, living to fight another day.

Use this as a buying opportunity.

Report

uchehapers |

February 15 12:16pm |

Permalink

“The ‘Abe market’ has run into its first major roadblock,” - really? fire up the printers, churn out more yen