Global Sports Media Market Outlook 2024-2030: Growth Drivers and Forecast

Executive Summary

The global sports media market reached USD 150 billion in 2024, but the audience is not the story. With over 4 billion viewers already watching, the real shift is rights value migrating from linear broadcast to streaming and Big Tech.

Key Market Velocity Data

- Current Market Value: USD 150 billion in 2024

- Projected Market Value: approximately USD 230 billion by 2030

- CAGR: about 7.5% during 2025 to 2030

- Dominant Segment: live sports broadcasting, US-led, consumer-driven

- Primary Growth Catalyst: the streaming and OTT shift, digital rights, and Big Tech entry

What Is Driving the Market?

Streaming is rewriting the economics. The market sits at USD 150 billion in 2024 and is projected toward USD 230 billion by 2030 at about 7.5% CAGR. Digital consumption is heading toward 1.5 billion users, while live events draw more than 4 billion viewers. Advertising and subscription revenue are both migrating toward digital platforms.

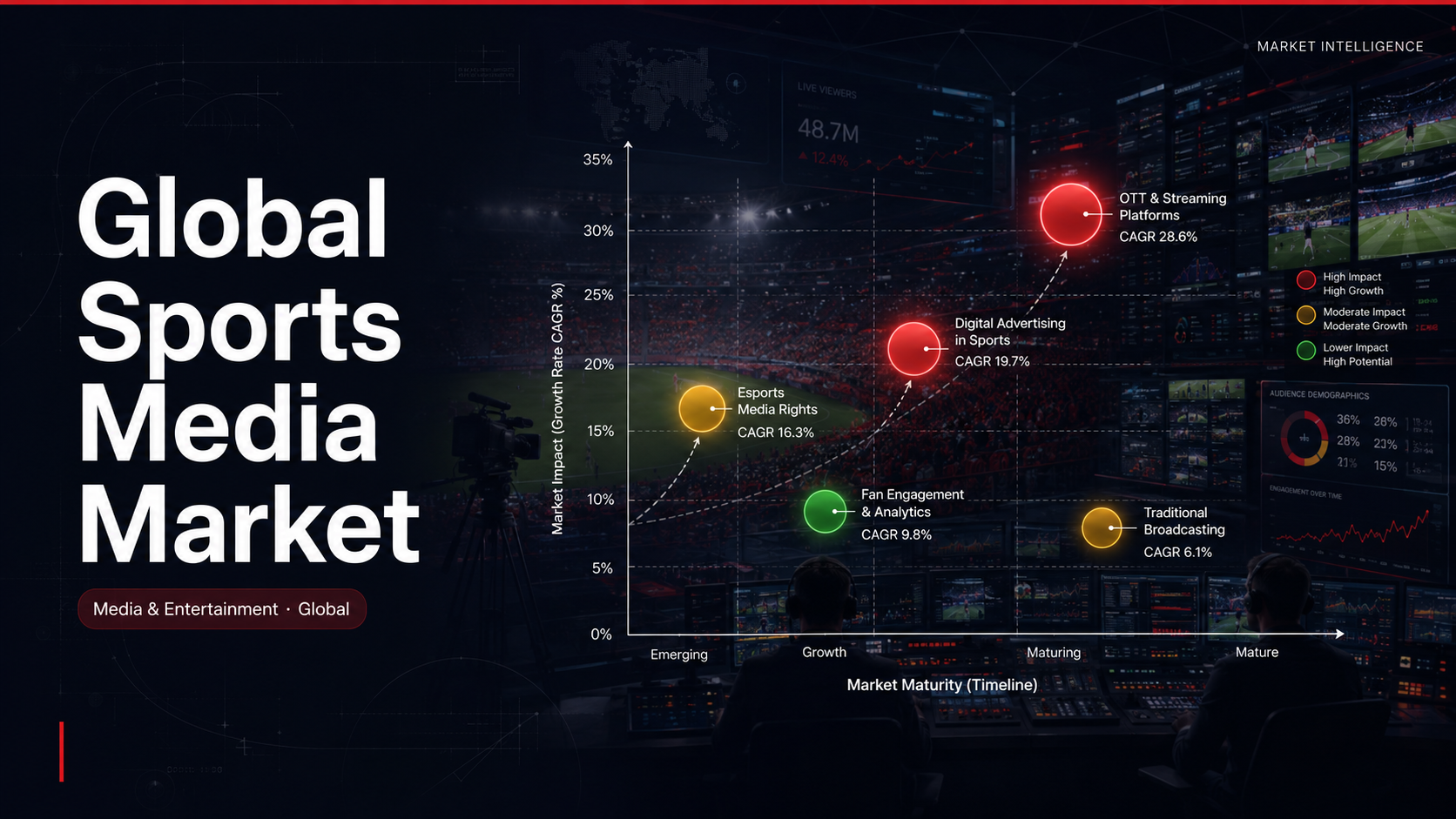

Rights value is the battleground. Broadcast rights still hold over 45% of revenue, but digital rights now exceed 25% and are climbing fastest. Streaming alone represents roughly USD 100 billion in revenue potential, drawing tech platforms into mega deals. This redistribution of value, not new viewership, is what reshapes the market.

- Audience scale: live sports draws more than 4 billion viewers, with 1.5 billion consuming digitally

- Rights shift: broadcast rights are over 45% of revenue, while digital rights now top 25%

- Streaming surge: sports OTT and streaming represent roughly USD 100 billion in revenue potential

- Big Tech entry: Amazon, YouTube, and Netflix are bidding aggressively for premium live rights

Which Entities Are Shaping the Market?

Traditional broadcasters still anchor the market. ESPN, NBC Sports, Fox Sports, CBS Sports, Sky, and Warner Bros. Discovery hold core rights, while DAZN, Paramount Global, and Tencent Sports extend globally. Together they shape the USD 150 billion market, where the United States leads roughly 38% on advertising and league value. Consolidation and joint streaming ventures are emerging as broadcasters defend scale.

Big Tech is the disruptor. Amazon Prime Video, YouTube TV, Netflix, and FuboTV are acquiring premium live rights, exemplified by the NFL's roughly USD 110 billion media-rights commitments through 2032 and Netflix's USD 150 million-a-year Christmas games. Individual consumers are the leading end-user, ahead of advertisers and sponsors. Each deal shifts a slice of audience and ad revenue from cable to streaming.

Oversight is fragmented across bodies. The Federal Communications Commission, the European Commission, and league authorities like the NFL and International Olympic Committee shape rights, antitrust, and broadcast rules. These frameworks govern how rights are packaged and sold across a market growing at about 7.5% from USD 150 billion.

How Do Segments and Regions Split?

Content and users concentrate value. Live sports broadcasting dominates by type, ahead of news, highlights, documentaries, and fast-rising esports. Individual consumers lead end-use, followed by advertisers and sports organizations, across the USD 150 billion market in 2024. Streaming-first formats are the fastest-growing segment. Short-form social clips and creator-led coverage are pulling younger audiences off traditional TV.

- By type: live broadcasting leads, while esports and short-form highlights grow fastest

- By user: individual consumers dominate, with advertisers and sponsors following

- By region: the United States leads near 38%, while APAC grows fastest

- By platform: streaming and OTT outpace linear broadcast in growth

What Does This Mean for B2B Decision-Makers?

Position for the streaming transition. The USD 150 billion market grows about 7.5%, but value is migrating to digital rights and direct-to-consumer streaming. Rights holders and platforms that lock premium live content will capture the shift, as broadcast-only models erode. Bundling sports with general entertainment is becoming the key subscriber-retention lever.

Tech scale is reshaping the bidding table. With Amazon, YouTube, and Netflix able to outspend legacy broadcasters, leagues are fragmenting rights across platforms. APAC, growing about 18.4%, is the fastest regional expansion lane for new entrants. Emerging markets and women's sports offer the highest-growth untapped rights pools.

- For broadcasters: defend premium live rights and build direct streaming products before Big Tech scales further

- For streaming platforms: bid for marquee live rights to drive subscriptions and engagement

- For leagues: fragment rights across platforms to maximize value, reach, and competitive bidding tension

- For investors: favor digital-rights and OTT exposure over linear-only broadcast assets

Ken Research Strategic Outlook

Ken Research sees global sports media as a rights-migration story, not an audience-growth one. The next phase is defined by streaming, digital rights, and Big Tech entry reshaping how premium content is sold and watched. Expect the USD 150 billion market to grow toward USD 230 billion by 2030 as OTT and digital rights outpace linear broadcast and Big Tech keeps bidding rights higher.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: Global Sports Media Market Report