Straddle and Strangle Options Strategies: Complete Beginner Guide

Most beginners learn options as directional bets: buy a call if bullish, buy a put if bearish. But what if you believe the market will make a big move but you do not know which direction? Or what if you believe the market will stay flat? Straddle and strangle strategies are built for exactly these situations – they let you trade volatility itself, independent of direction.

This guide explains both strategies simply, shows when each one works, and highlights the risks that most guides gloss over.

The Long Straddle: Betting on a Big Move (Either Direction)

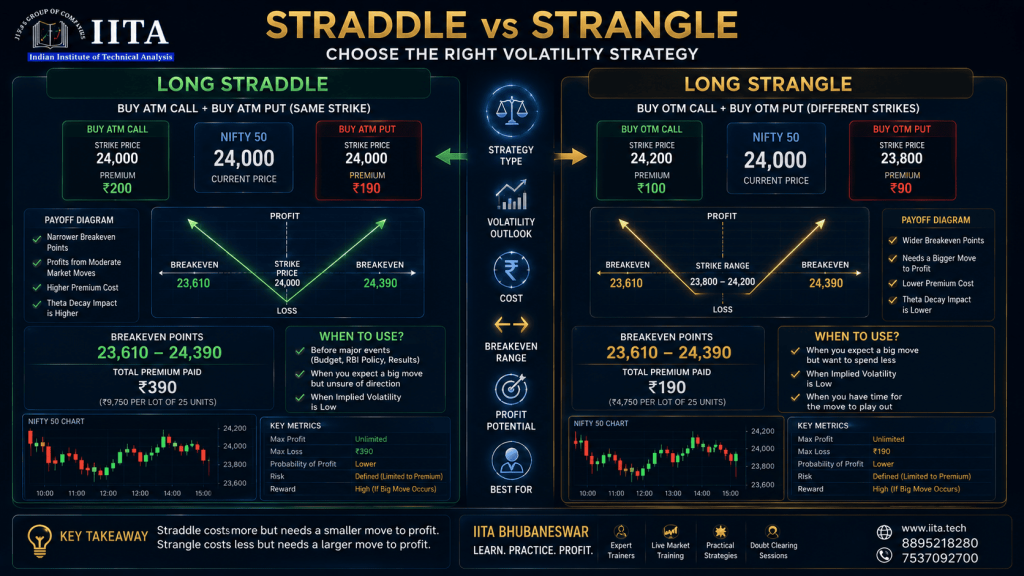

A long straddle means buying both a call option and a put option at the same strike price and same expiry. You pay premium for both.

Example: Nifty is at 24,000. You buy the 24,000 call for ₹200 and the 24,000 put for ₹190. Total cost: ₹390 per unit (₹9,750 per lot of 25 units). You now profit if Nifty moves more than 390 points in either direction before expiry. A move to 24,500 makes the call profitable enough to cover both premiums. A crash to 23,500 makes the put profitable enough.

When to Use a Long Straddle

- Before a major event (budget, RBI policy, election results) where a large move is expected but the direction is uncertain

- Before earnings announcements for individual stocks

- When implied volatility is low and you expect it to spike (making both options more valuable)

The Risk of Long Straddles

The risk is that the big move never comes. If Nifty stays near 24,000, both options lose value from Theta decay, and you lose the entire premium paid. This is the most common outcome because events often produce smaller moves than expected, or the expected move is already priced into the options (high IV). The market needs to move MORE than the total premium paid to profit. Long straddles before well-anticipated events often fail because IV is already high, making the options expensive.

The Long Strangle: A Cheaper Volatility Bet

A long strangle is similar to a straddle but uses different strike prices – typically an out-of-the-money call and an out-of-the-money put. This makes it cheaper than a straddle but requires a larger move to profit.

Example: Nifty at 24,000. You buy the 24,200 call for ₹100 and the 23,800 put for ₹90. Total cost: ₹190. Cheaper than the straddle, but now Nifty needs to move beyond 24,390 or below 23,610 to profit. The breakeven points are wider apart.

Straddle vs Strangle: Which One?

- Straddle: higher cost, narrower breakeven, profits from moderate moves

- Strangle: lower cost, wider breakeven, needs a larger move to profit

- Both: lose money if the market stays flat – Theta decay eats both legs

The Short Straddle: Betting on the Market Staying Flat

A short straddle means selling both a call and a put at the same strike price. You collect premium upfront and profit if the market stays near that strike until expiry, because both options lose value from Theta decay. Your maximum profit is the total premium collected.

The risk is unlimited in theory. If the market makes a large move in either direction, your losses can be substantial. Short straddles require significant margin, strict risk management, and experience. They are professional strategies, not beginner trades.

The Short Strangle: Wider Safety Zone

A short strangle means selling an OTM call and an OTM put, collecting premium on both. It profits if the market stays between the two strike prices. The wider the strikes, the higher the probability of profit but the lower the premium collected.

Example: Sell the 24,300 call and the 23,700 put. You profit if Nifty stays between 23,700 and 24,300. The premium collected is your maximum profit; the risk is a breakout beyond either strike. Short strangles are popular among experienced traders for weekly income but require careful position sizing and adjustment skills.

Key Concepts for Straddle/Strangle Trading

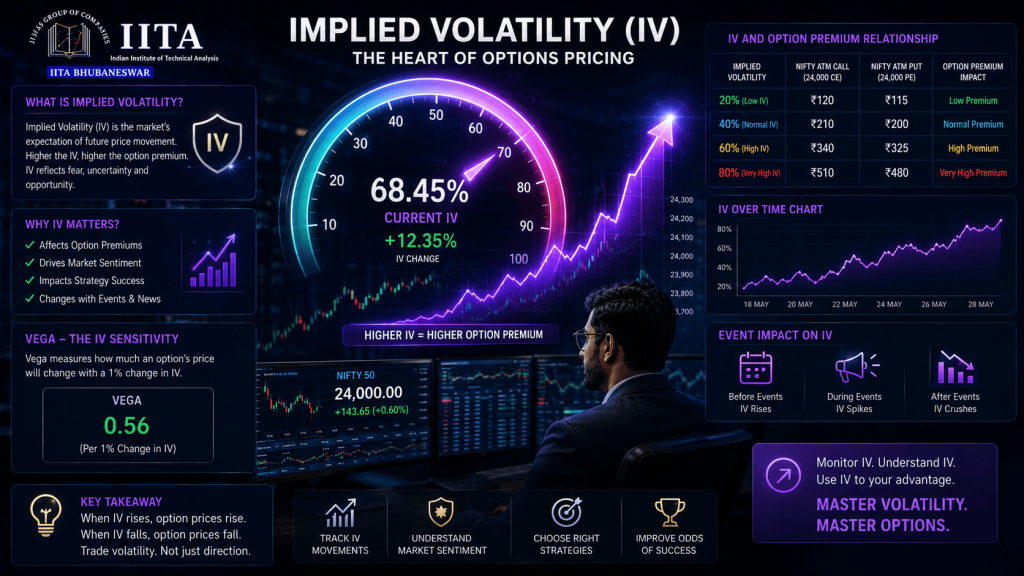

Implied Volatility (IV) Is Everything

These strategies are fundamentally volatility trades. Long straddles and strangles benefit from rising IV (options become more valuable). Short straddles and strangles benefit from falling IV (options lose value faster). Buying a straddle when IV is already high – the classic beginner mistake before events – means you pay inflated prices and need an even larger move to profit.

IV Crush After Events

After an event, IV typically drops sharply regardless of what happens (“IV crush”). Long straddle holders often find that even though the market moved, the IV drop destroyed the option value. Short straddle holders benefit from this crush. Understanding this asymmetry is critical before placing any event-based straddle trade.

Timing: When to Enter and Exit Straddles

Timing is everything with these strategies. For long straddles, the ideal entry is when implied volatility is relatively low and you expect it to rise – typically several days before a major event, not the day before when IV has already spiked. For exit, set a profit target rather than holding to expiry, because Theta decay accelerates as expiry approaches. If the big move happens early, take profit; if the event is imminent and the move has not happened, cut losses before the final Theta collapse.

For short straddles and strangles, the ideal entry is when IV is high and expected to drop – typically right after an event when the uncertainty that inflated IV has resolved. Theta works in your favour daily, so patience is your edge. Monitor your positions for any sudden moves that approach your breakeven points and have adjustment plans (rolling or closing one leg) prepared before you need them.

Common Mistakes

- Buying straddles before events when IV is already elevated (paying too much)

- Not calculating the breakeven points before entering – you need the move to exceed total premium

- Holding long straddles too long and letting Theta decay destroy both legs

- Selling straddles without understanding the unlimited risk or having adjustment plans

- Ignoring the Vega component – IV changes affect these strategies more than most

Frequently Asked Questions

What is the difference between straddle and strangle?

A straddle uses the same strike price for both call and put (costs more, narrower breakeven). A strangle uses different strike prices – OTM call and OTM put (costs less, wider breakeven). Both profit from big moves when bought and from flat markets when sold.

Is a straddle a good strategy for beginners?

Long straddles are straightforward to understand but difficult to profit from because of Theta decay and IV dynamics. Short straddles involve unlimited risk. Beginners should paper trade these strategies extensively before using real capital and fully understand Greeks before attempting them.

Can I trade straddles on Nifty?

Yes. Nifty options are among the most liquid in the world, making straddles and strangles easy to execute. Weekly expiry options are commonly used for short-term straddle strategies. However, weekly options have accelerated Theta, making timing critical.

Learn Straddle, Strangle and Advanced Options Strategies with IITA Bhubaneswar

At IITA (Indian Institute of Technical Analysis), Bhubaneswar, concepts like these are not taught from slides alone. Our trainers demonstrate on live market charts, letting you practise in real conditions with mentor guidance.

- Live market sessions – learn by doing, not just watching

- Experienced traders as trainers who practise what they teach

- Small batches for personal attention and doubt-clearing

- Post-course mentorship so support continues after class ends

- Classroom and online options available across Odisha

Visit iita.tech or call us to book a free introductory workshop.

Disclaimer: Stock market trading involves financial risk. This article is for educational purposes only and is not investment advice.