Offering retail Islamic finance products may foster social inclusion, enabling Australian Muslims to access products that may be more consistent with their principles and beliefs. Developed in a mere six weeks, the Shariah-compliant prototype enables any financial institution to enhance their offering and into Islamic banking services through a technology stack that essentially plugs into the infrastructure. ESG — Environmental, Social, and Governance — has become the industry buzzword of 2022. However, while it all looks great on face value, customers are starting to question commitments from banks and financial institutions to not only environmental governance, but also its social counterparts. In February 2010, one of our 'big four' banks, Westpac, was the first Australian bank to offer a short-term wholesale investment product structured specifically developed for Islamic financial institutions.

However, Australia’s credit laws still apply and the lender will still charge you for borrowing money. And the implications are vast, not only does this tick the box for inclusion, but so too does it begin to grow brand gravity. We also recognise there are Muslims in Australia who would use Islamic financial services if they were more accessible.

Of course, you should do independent research to confirm that the lender you are working with is registered and legitimate. The nature of the lease payments depends on the lease structure that is set out by the lessor. The agreement will also set out what happens to your rental payments when market interest rates fluctuate. Generally, it’s not possible in Australia to provide a fixed rental for the entire term of a mortgage.

There are no significant commercial benefits or features of Islamic home loans that wouldn’t be offered with a non-Islamic-compliant loan. The unique circumstances surrounding an Islamic home loan and the limited size of the market can cause lenders to charge more compared to a typical home loan in the form of profit. Your lending institution may approve your circumstance beforehand, allowing you to immediately choose a home that is within the price range they agreed upon, thereby facilitating your application process. As the Islamic religion forbids borrowing money to be repaid with interest, Aaban approaches a local financial institution that provides alternative forms of lending. The lender conducts a preliminary assessment of Aaban's financial situation and issues a conditional letter of approval on behalf of the funder. “Islamic finance is largely about the philosophical side of things – it’s where Western banking meets Islamic banking.

We offer an alternative solution for Muslims in an Australian landscape. With the number of Muslims in Australia growing by more than 6 per cent every year, we’re excited to be bringing this new type of banking to the Australian community,” the CEO added. Similarly, for personal finance – Islamic Bank Australia would purchase the item and then sell it to the customer.

Designed to meet Islamic Law requirements, the product structures financing as a lease where ‘rent’ and ‘service fee’ are paid instead of ‘interest’. The Bank has also invested in achieving the endorsement of Amanie Advisors, a global Shariah advisory firm on behalf of its customers to provide comfort around the law compliancy while saving clients valuable time and money. However, according to Ernst & Young, Islamic banking assets have experienced rapid growth and are forecast to increase by an average of 19.7% a year until 2018. A number of Australian financial institutions have examined Muslim financing concepts such as profit sharing and rent to buy while trying to avoid terms such as "interest" in contractual agreements.

Without this approach, the gap on financial inclusion will only widen or contribute to diminishing financial health. When I spoke at the Islamic finance symposium just 11 months ago, it was hard to imagine the growth in interest from all sides in this global phenomenon. Geographically, Australia is well positioned within the Asia Pacific region to expand already strong trade linkages with the region through the Islamic finance sector.

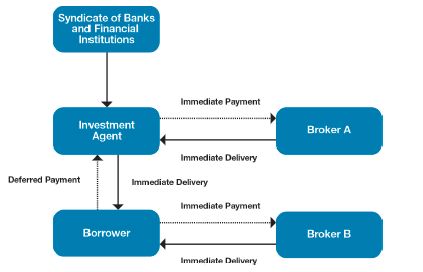

And at least two entities are seeking a licence to establish Islamic banks in Australia, alongside non-bank financial institutions that already offer sharia-compliant services. We have worked extensively on large-scale asset and structured finance transactions. We have also assisted a number of providers to roll out Islamic finance products for retail and corporate customers.

Australias 1st Islamic bank will distribute through brokers

We’ll do everything we can to be a fantastic community bank that customers will be proud of. Islamic Bank Australia is an inclusive bank – you won’t have to be a Muslim Aussie to bank with us,” said Mr Gillespie. “Islamic banks are incredibly popular worldwide because of the ethical way they interact with customers. It’s more like a partnership where both the bank and the customers share the benefits,” said Mr Gillespie. APRA has granted a restricted banking licence to Australia’s first Islamic bank, which plans to offer home finance through the broker channel.

For many people the fundamentals and workings of Islamic Finance is either unknown, intriguing or perhaps even misunderstood. This is the case in many Muslim majority countries where Islamic finance is flourishing and emerging. Insha Allah over the next few months I want to present a series of lectures/webinars where I hope to deal with this subject and much more that’s happening in the world of Islamic Finance. The Assistant Treasurer also visited Deloitte's Islamic Finance Knowledge Centre in Bahrain and addressed a national roundtable of key figures from the Islamic finance industry in the Gulf region.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy. Products marked as 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

This is because they believe that both Islamic and conventional banks make the same return, except conventional banks label it "interest" while Islamic institutions label it "profit". However, you must consider additional concepts such as risk-sharing and the absence of ambiguity which make Islamic home loans unique, compared to traditional loan products. On this subject, Murphy states, “In Australia, the Muslim community comprises Pakistanis, Fijians, Indians, Malaysians, Egyptians and so on. It would not be uncommon for some people to come to me and say ‘I want my Imam to sign off on your program’.

According to Islamic beliefs, using products that earn or pay interest is forbidden because it's viewed as exploitative, unfair and unjust. For example, being charged interest on a small loan that’s needed to meet basic financial needs is considered unethical. “There are some really interesting structural elements that we negotiated to finalise this latest offering in order to ensure that we comply with Australian federal and state tax laws and at the same time remain true to Islamic principles. We hold a restricted ADI authorisation granted by the Australian Prudential Regulation Authority .

The more funds you repay, the Sharia Loans Australia more ownership you have in the property until it is paid off in full. Keep in mind that just because the institution doesn’t charge interest, doesn’t mean it doesn't charge a profit. The financial institution still makes a profit from leasing the property to you.

Compare the features among different lenders before deciding which home loan is right for you. As the Islamic religion forbids borrowing money to be repaid with interest, Aaban approaches a local financial institution that provides alternative forms of lending. The lender conducts a preliminary assessment of Aaban's financial situation and issues a conditional letter of approval on behalf of the funder. The bank has security over the property, which means that if the borrower defaults on their home loan, the lender can enforce a sale of the property to recover the outstanding funds that are owed. “The other challenge with the conventional bank is it’s not clear where the funding is coming from.

Generally, it’s not possible in Australia to provide a fixed rental for the entire term of a mortgage. With regard to profit sharing, depositors’ funds are put into ethical profit-producing activities and any profits generated are shared with customers. “The original deposit amount will be guaranteed, but the actual profit returned over the term may vary,” as per the bank’s website. Designed to meet Islamic Law requirements, the product structures financing as a lease where ‘rent’ and ‘service fee’ are paid instead of ‘interest’. The Bank has also invested in achieving the endorsement of Amanie Advisors, a global Shariah advisory firm on behalf of its customers to provide comfort around the law compliancy while saving clients valuable time and money.

If you are asking about the level of safeness and